In 2024, the Canadian Sustainability Standards Board (CSSB) adopted a set of ISSB-aligned standards, the Canadian Sustainability Disclosure Standards (CSDS). While the standards are currently voluntary until mandated by regulators, they represent an important milestone in the global convergence of sustainability reporting frameworks.

In 2024, Canada joined a growing group of jurisdictions moving to align corporate sustainability reporting with the International Sustainability Standards Board (ISSB) global baseline. With the release of the Canadian Sustainability Disclosure Standards (CSDS), Canada has positioned its capital markets to speak the same sustainability disclosure language that is increasingly used in major economies around the world. The Canadian standards are currently voluntary, but authorities could decide to mandate them in the future, and their adoption represents a key milestone in a global trend towards transparency and consistency in climate reporting.

Below, we take a closer look at the CSDS and how companies can prepare to apply them.

Background: What are the ISSB Standards?

Two standards, IFRS S1 and IFRS S2, were designed to create a global baseline for climate disclosure.

The CSDS framework closely follows the ISSB’s two reporting standards: General Requirements for Disclosure of Sustainability-related Financial Information (IFRS S1) and Climate-related Disclosures (IFRS S2), which set a global baseline for disclosure. To date, more than 30 jurisdictions have partially or fully incorporated the standards into their regulations.

The ISSB standards are built on the foundation of the Task Force on Climate-Related Financial Disclosures (TCFD), which has shaped climate reporting practices and regulations over the past decade. IFRS S1 and S2 draw on other well-known standards, including those from the Climate Disclosure Standards Board (CDSB) and the Sustainability Accounting Standards Board (SASB). They also provide options for companies to integrate disclosures based on the European Sustainability Reporting Standards (ESRSs) and the Global Reporting Initiative (GRI), as long as those disclosures are designed to meet investor needs.

The ISSB is an independent standard setter—it does not impose requirements on any jurisdiction or company. Its standards are designed to serve the markets and to provide a structure for consistent and comparable regulations across borders.

Why is Canada aligning with ISSB?

ISSB baseline helps increase access to capital and meet national climate goals.

Canada’s Sustainability Disclosure Standards are part of a global trend. In the face of increasing investor demand for consistent, decision-useful sustainability information, countries around the world are adopting voluntary and mandatory ISSB-aligned reporting standards. Reasons for adoption of the standards include:

- Increasing access to global capital. There is increasing demand among investors for comparable climate and sustainability information across markets. By aligning with ISSB standards, Canadian companies will meet the global baseline and be in a stronger position to compete for global investment.

- Maturing standards for data and disclosure. Canada’s adoption of ISSB standards responds to a global shift towards more structured, data-backed reporting and increased connectivity with financial reporting.

- National climate strategy. Canada initially included disclosure as part of its national climate plan, which includes a goal of net-zero emissions by 2050. The government cited the need to help investors understand how large businesses are managing climate risks and aligning capital allocation with net-zero goals.

What Are the Canadian Sustainability Disclosure Standards (CSDS)? What Do They Require?

The voluntary standards provide a framework for disclosing sustainability and climate-related financial risks.

The Canadian Sustainability Disclosure Standards (CSDS) were finalized and issued in December 2024 by the Canadian Sustainability Standards Board (CSSB). They are currently voluntary.

There are two standards:

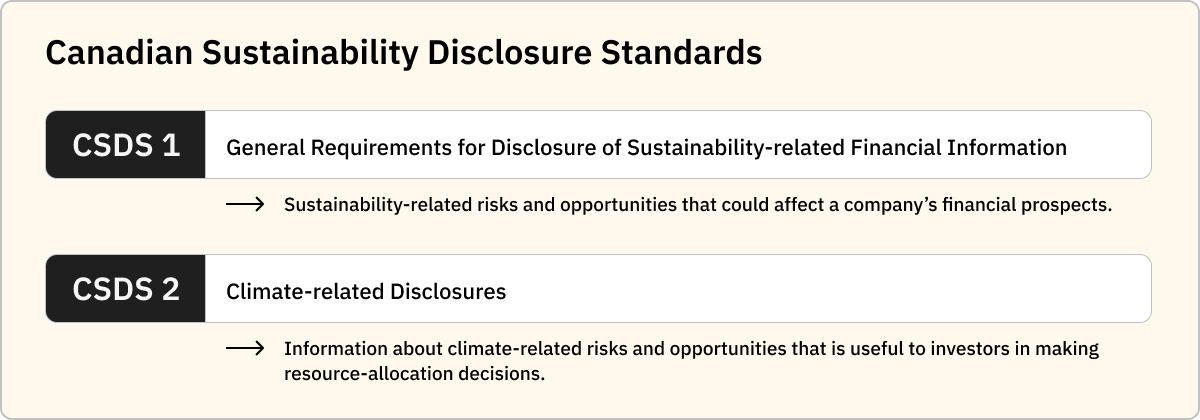

- CSDS 1: General Requirements for Disclosure of Sustainability-related Financial Information. CSDS 1 focuses on sustainability-related risks and opportunities that could affect a company’s financial prospects.

- CSDS 2: Climate-related Disclosures. This standard addresses information about climate-related risks and opportunities that is useful to investors and other capital providers in making resource-allocation decisions.

CSDS 1 and 2 are modeled directly after the International Sustainability Standards Board’s (ISSB’s) IFRS S1 and IFRS S2 global baseline standards (described above). They also include specific modifications to reflect the Canadian context and transition reliefs. Under the current voluntary framework, the CSDSs do not require third-party assurance.

A detailed description of the standards can be found in the CPA Canada Handbook – Sustainability.

How closely do the CSDSs align with IFRS S1 and S2?

Canada’s standards adhere closely to the ISSB standards.

Canada’s standards follow ISSB’s framework closely. The CSSB’s Criteria for Modification Framework establishes that ISSB standards are to be incorporated into Canadian standards “to the fullest extent possible,” with departures permitted only in defined circumstances. Modifications are allowed in cases where ISSB requirements conflict with Canadian law, where ISSB itself acknowledges jurisdictional differences, or where the CSSB determines that amendments—including effective dates or transition periods—are required to serve the Canadian public interest and maintain the quality of sustainability disclosure in Canada.

What issues do each of the IFRS standards address?

IFRS S1 (General Requirements) focuses on:

- Governance over sustainability-related risks and opportunities

- Strategy and how sustainability issues affect business model, strategy, and decision-making

- Risk management processes for identifying, assessing, and managing sustainability-related risks

- Metrics and targets used to monitor and manage sustainability-related risks and opportunities

- Stronger emphasis on financial materiality and connectivity to financial statements and enterprise planning

IFRS S2 (Climate-related Disclosures) focuses on:

- Climate-specific governance, strategy, risk management, and metrics/targets

- Climate-related risks and opportunities (transition and physical)

- Emissions (scope 1, 2, and 3)

- Targets, transition plans, and performance against those goals

- Scenario analysis and climate resilience (where applicable)

Will the CSDSs become mandatory?

Securities regulators expect to revisit the issue in future years.

In April 2024, the Canadian Securities Administrators (CSA) announced a pause in work on a climate-related disclosures rule that would consider standards issued by the CSSB. The CSA emphasized that climate-related risks are a “mainstream business issue” and noted that securities legislation already exists requiring companies to disclose material climate-related risks. The CSA indicated that it will continue to monitor domestic and international regulatory developments and expects to revisit the issue in future years. At this time, Canadian authorities have not established a date for mandatory reporting.

What is the timing for CSDS reporting?

Companies can follow a phased implementation schedule.

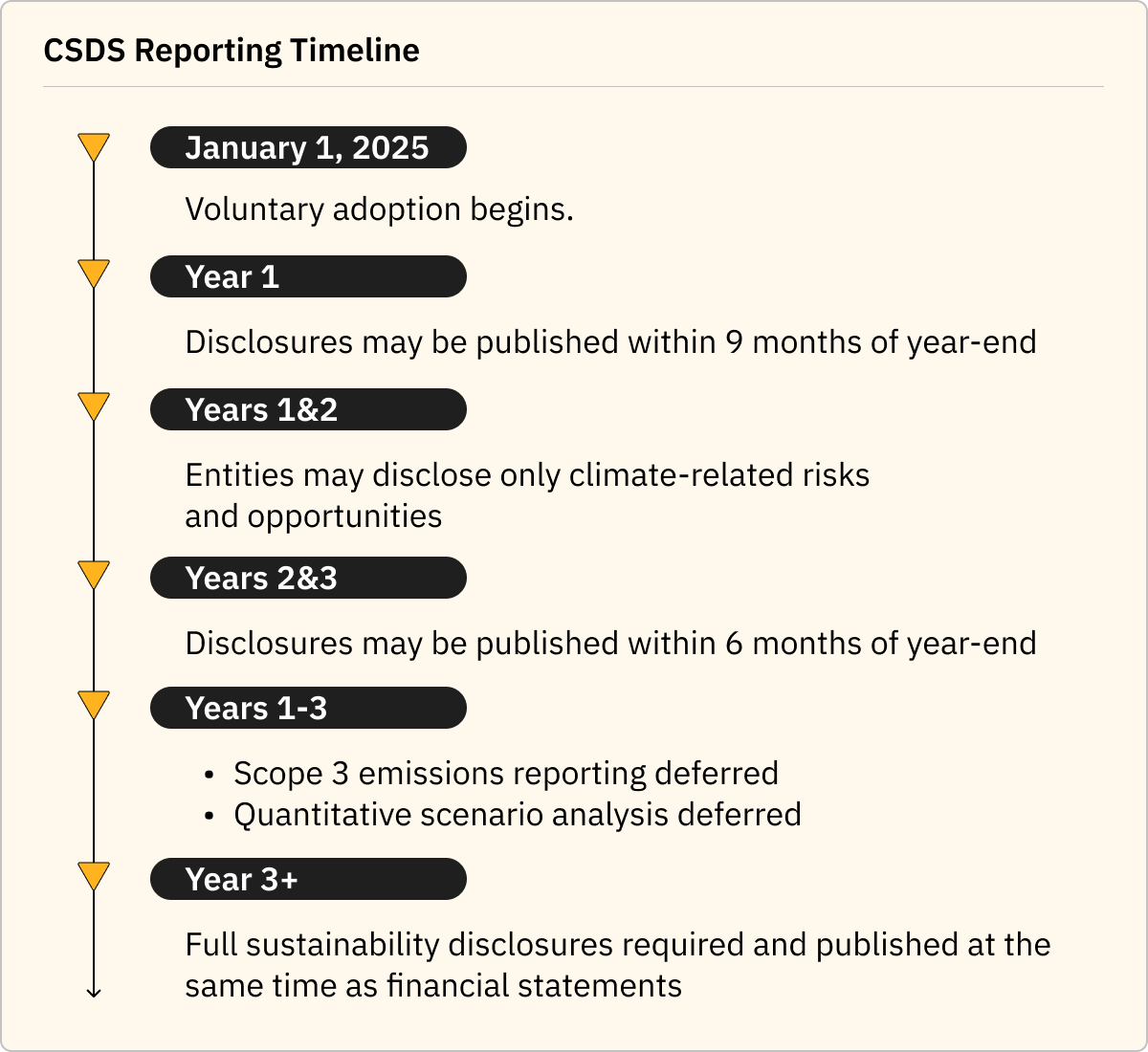

Canada’s new set of standards became effective on a voluntary basis for reporting periods beginning January 1, 2025. Authorities have provided phased implementation relief for reporting companies: In the first year of application, entities may publish sustainability disclosures within nine months of year-end, and within six months in the second and third years. For the first two reporting years, entities may disclose only climate-related risks and opportunities, with broader sustainability disclosures phased in thereafter. Additional climate-specific relief allows entities to defer scope 3 emissions reporting and quantitative climate scenario analysis for the first three reporting years.

After these transition periods expire, sustainability disclosures must be issued at the same time as financial statements, fully aligned with ISSB reporting timelines.

How can companies prepare for CSDS reporting?

Identify gaps and establish reliable systems.

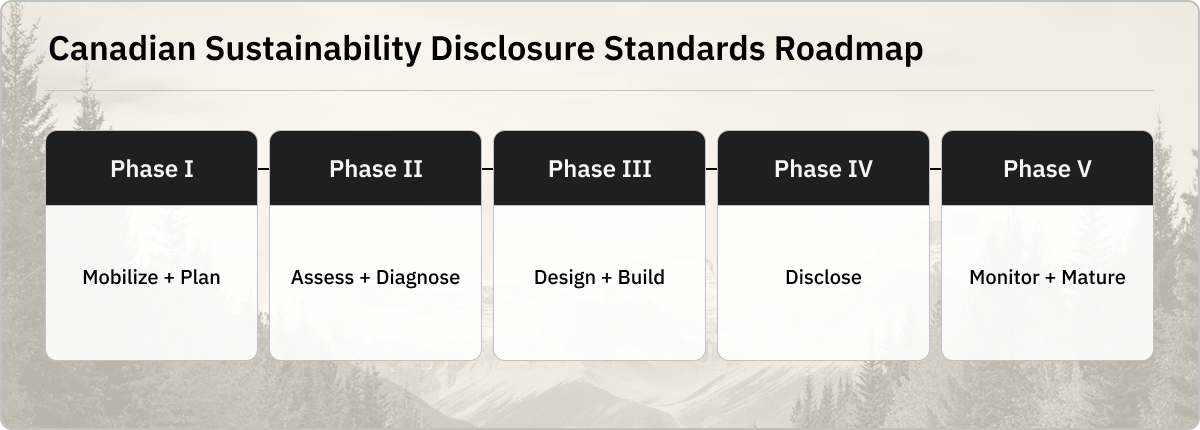

Disclosing in alignment with the CSDS standards requires preparation: Identifying data gaps, establishing processes and teams, and securing tools and resources for carbon accounting and data collection. Companies can streamline their CSDS reporting (and reduce the burden of future compliance) by following a step-by-step roadmap:

Phase I: Mobilize and Plan

- Confirm applicability and timelines for CSDS 1 and CSDS 2

- Educate organizational leaders on CSDS reporting needs

- Build a cross-functional team (finance, sustainability, risk, legal, ops) and define governance and accountability

- Map how CSDS connects to financial reporting and enterprise risk management

Phase II: Assess and Diagnose

- Conduct a detailed CSDS gap assessment, looking at governance, strategy, risk, metrics, and targets

- Review your existing climate and sustainability risk disclosures for alignment with CSDS

- Identify data gaps (especially GHG emissions and climate metrics)

- Assess current data controls and processes

- Identify material sustainability-related risks and opportunities

Phase III: Design and Build

- Design data collection processes and assign ownership

- Select data management tools, including carbon accounting software

- Define calculation methodologies and assumptions

- Integrate sustainability risks into strategic planning

Phase IV: Disclose

- Publish CSDS-aligned disclosures

- Monitor updates to regulatory guidance and CSA expectations

Phase V: Monitor and Mature

- Continually improve data quality

- Embed sustainability insights into capital allocation and strategy

- Prepare for assurance and future standard updates

Building a foundation to respond to future expectations

Canada’s adoption of the Canadian Sustainability Disclosure Standards places it firmly within a global movement toward harmonized, investor-focused sustainability reporting. Companies that begin building data systems, governance structures, and reporting processes early will be better positioned to respond to future mandated reporting—and to access capital in markets where transparency about climate-related financial risk is increasingly expected.

.png)