The Partnership for Carbon Accounting Financials (PCAF) is a global initiative that supports financial institutions in measuring the greenhouse gas emissions associated with their investments and loans. The organization’s Global GHG Accounting and Reporting Standard (PCAF Standard) provides guidance to help calculate and report these financed emissions. In December 2025, PCAF made substantial updates to the standard.

The Partnership for Carbon Accounting Financials (PCAF) was established in 2015 by a group of Dutch banks, with the goal of harmonizing the measurement and disclosure of greenhouse gases across the financial sector.

The global initiative helps financial organizations understand and disclose indirect emissions generated by their investments and loans. These financed emissions typically make up the vast majority of a financial institution’s carbon footprint—often more than 90 percent.

In 2020, responding to industry demand, PCAF created the Global GHG Accounting and Reporting Standard for the Financial Industry (PCAF Standard). The standard was updated in December 2025, with expansions to methodologies, reporting, and asset classes.

In this guide, we’ll cover what PCAF is, its goals, and how it aligns with other initiatives and organizations. We’ll also provide an overview of the PCAF Standard, including the 2025 updates.

What is PCAF?

The industry-led initiative helps financial institutions disclose emissions.

PCAF is a worldwide collaboration of financial institutions that provides a streamlined process to review and disclose financed emissions—the greenhouse gases indirectly generated as a result of investments and loans (e.g., banks indirectly create financed emissions by financing fossil fuel companies).

PCAF’s mission is to promote the financial industry’s alignment with the Paris Agreement. To do this, they set goals to create a global accounting standard (which they’ve achieved with the PCAF Standard) and to get more than 250 financial institutions to review and disclose their financed emissions (which they’ve surpassed). PCAF also created the Strategic Framework for Paris Alignment. This document helps financial institutions understand how they can align with the Paris Agreement and other global climate finance initiatives.

Financed emissions are notoriously difficult to measure; calculating them requires data from a variety of other businesses in the value chain, many of which may not be actively measuring their carbon footprint.

What is the PCAF Standard?

The PCAF Standard provides methodological guidance for reporting emissions.

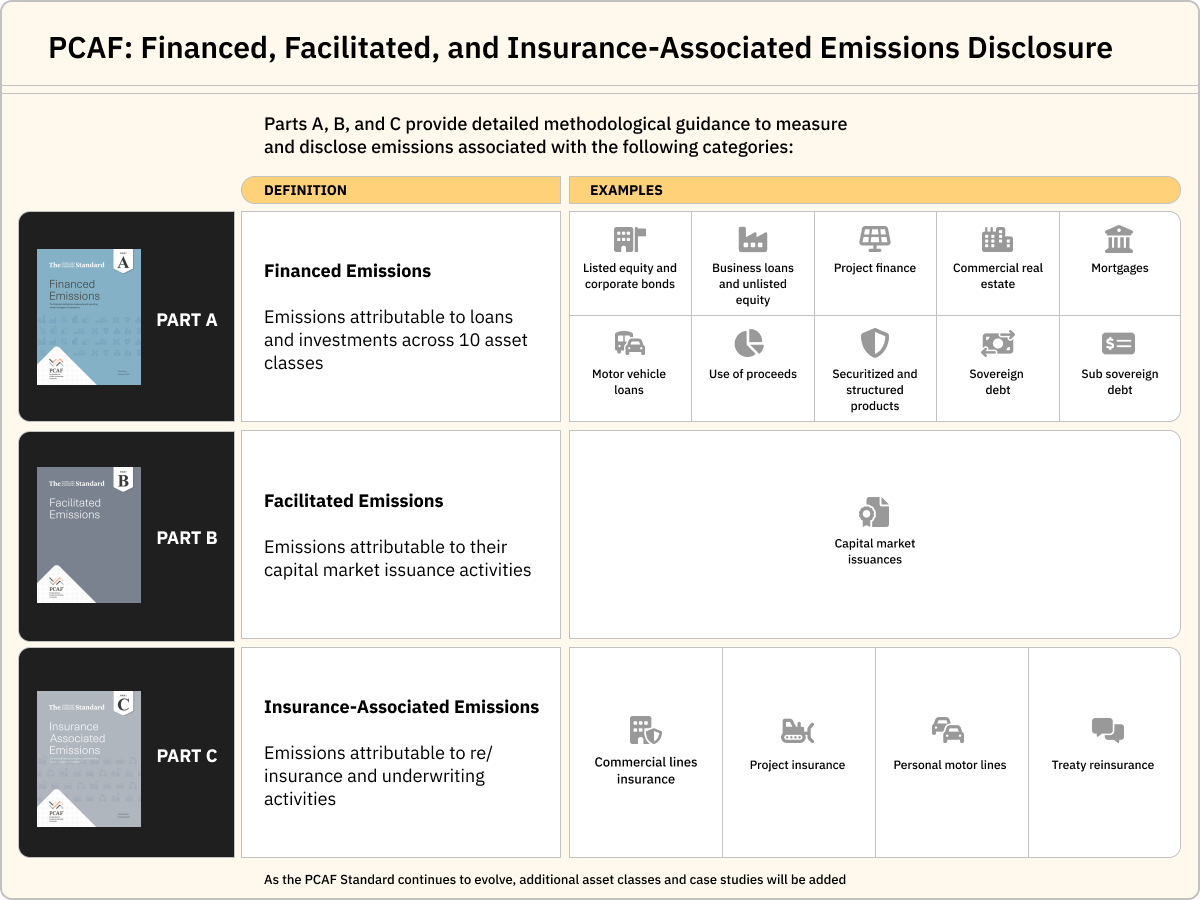

PCAF’s Global GHG Accounting and Reporting Standard provides a set of guidelines to help financial institutions measure and report greenhouse gas emissions associated with their financial activities. The PCAF Standard provides detailed methodological guidance for three categories: Financed Emissions (Part A), Facilitated Emissions (Part B), and Insurance-associated Emissions (Part C).

These are emissions attributable to loans and investments across 10 asset classes.

These are emissions attributable to capital market and issuance activities.

Part C: Insurance-Associated Emissions

These are emissions attributable to re-insurance and underwriting activities

Updates to the PCAF Standard

In December 2025, PCAF announced updates to its guidance for Scope 3 Category 15 (Part A: Financed Emissions and Part C: Insurance-associated Emissions). The changes expand methodologies and coverage and introduce new metrics. Key changes include:

Expanded coverage

- Addition of new asset class methodologies (Use of Proceeds, securitization, sovereign and sub-sovereign debt)

- Expansion of insurance coverage to project insurance and treaty re-insurance

New methodologies

- Use of Proceeds (UoP): Allows lenders to account for specific assets financed under UoP debt or equity structures

- Differentiation between the roles of issuers and investors

- New methodologies for securitization, sub-sovereign debt, and undrawn loan commitments

New reporting elements

- Fluctuation analysis

- Inflation adjustments (Consumer Price Index)

New metrics

- Financed avoided emissions/climate solutions (separate from Scopes 1–3)

- Forward-looking metrics: Expected Emissions Reductions (EER) and Expected Avoided Emissions (EAE)

Insurance expansion (Part C)

- Project insurance: premium-based attribution

- Treaty reinsurance: data-based (Method A) or proxy-based (Method B)

The 2025 updates reflect a move toward more comprehensive and expanded reporting coverage, while also highlighting ongoing challenges around complexity and data dependency. PCAF has noted that, while it is advancing toward more complete financed emissions accounting, effective implementation will depend on improvements in data quality and availability.

What are the PCAF asset classes?

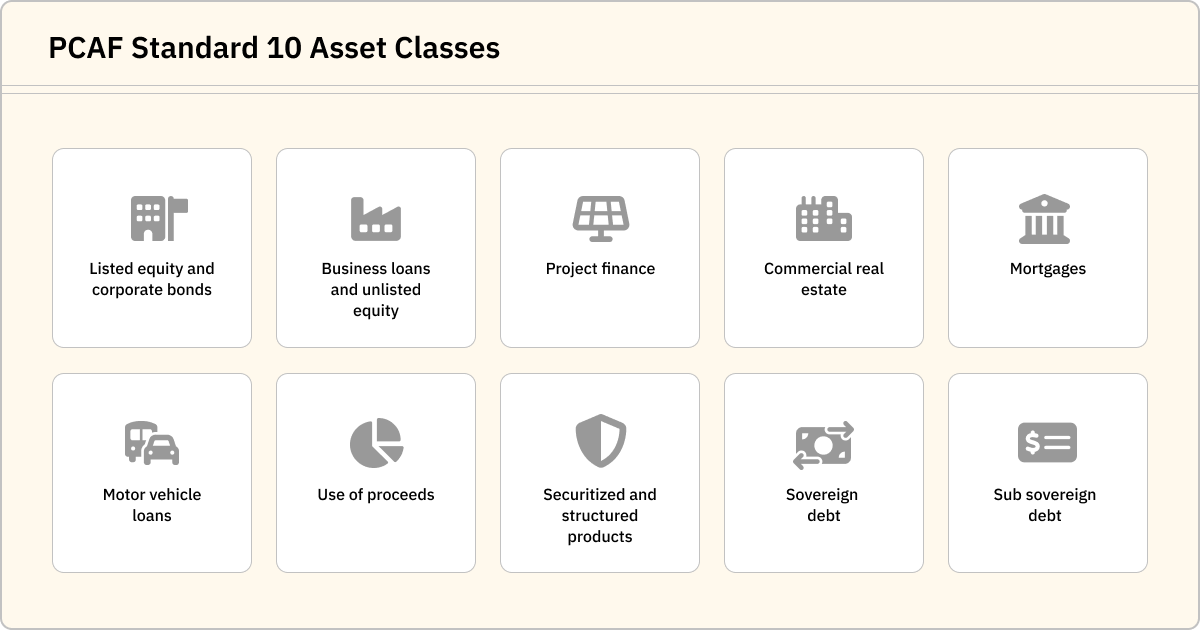

PCAF now focuses on 10 asset classes.

The PCAF methodology initially covered six investment categories. With the 2025 updates, methodologies for four new asset classes were added, bringing the total to ten. The PCAF Global Core team selected asset classes by identifying the most common classes for financial institutions around the world.

The ten asset classes are:

- Listed equity and corporate bonds

- Business loans and unlisted equity

- Project finance

- Commercial real estate

- Mortgages

- Motor vehicle loans

- Use of Proceeds (UoP) structures

- Securitizations and structured products

- Sovereign debt

- Sub-sovereign debt

PCAF requires institutions to disclose the percentage of their current total investments and loans in their financed emissions inventory covered by these asset classes. This requirement allows institutions to highlight any data limitations on their end or constraints as a result of a gap in PCAF’s framework.

How is the PCAF standard implemented?

Regional teams work to advance implementation around the world.

PCAF’s regional implementation teams in North America, Latin America, Europe, Africa, and Asia-Pacific help implement the PCAF Standard in their respective areas. Each team has its own form of governance and works to create specific local guidelines. Some regional teams may eventually work in national teams to tailor implementation to the needs of different countries and jurisdictions.

How does PCAF partner with other organizations and initiatives?

PCAF aligns with leading disclosure frameworks.

As an industry-led initiative, PCAF works with other organizations and initiatives to promote consistency. The PCAF Standard complements leading recommendations like those from the International Sustainability Standards Board (ISSB) and Task Force on Climate-Related Financial Disclosures’ (TCFD).

Aligning existing and widely used protocols and recommendations helps streamline the process and create comparable disclosures. Alignment also makes it easier for institutions to benchmark progress against peers, ensure high-quality data, and reduce redundancy as many organizations, initiatives, and jurisdictions continue looking for ways to improve their carbon management as a whole. Key alignments include:

Carbon Disclosure Project (CDP)

CDP and PCAF have aligned their data quality frameworks. Since 2022, CDP's data quality scoring methodology has been aligned to PCAF's data quality scores for listed equity and corporate bonds, allowing users of CDP's Full GHG Emissions Dataset to utilize it for reporting financed emissions with an added weighted PCAF Data Quality Score. PCAF is also CDP's recommended framework in its financial sector questionnaire, and the two organizations collaborate on capacity-building workshops and joint publications.

Greenhouse Gas Protocol (GHGP)

PCAF’s framework earned a “Built on GHG Protocol” mark, meaning that it conformed to and aligned with the requirements set forth in Scope 3 Category 15. In addition, the PCAF Standard continues to follow GHGP’s five core principles: completeness, consistency, relevance, accuracy and transparency.

Task Force on Climate-Related Financial Disclosures (TCFD)

PCAF’s framework also aligns with the TCFD’s recommendations for financial institutions. One of the TCFD’s goals is for reporting organizations to measure and disclose policy-related transition risks. An example of a transition risk would be a potential carbon tax for heavily emitting industries, which would result in high operational costs for power plants and other fossil fuel companies. Measuring financed emissions and their associated value helps bring financial institutions closer to understanding their risk level. It also helps institutions identify their next steps, like prioritizing their carbon “hot spots” and building transition plans.

Paris Agreement Capital Transition Assessment (PACTA)

PCAF focuses on measurement and disclosure, while PACTA supports the steps that follow: target setting, scenario analysis, and strategy development. Institutions can use PACTA to assess how their portfolio currently aligns with the Paris Climate Agreement. PACTA for Investors is well-suited for those implementing PCAF's methodology for equity and corporate bonds; PACTA for Banks is a fit for lending portfolios.

Science-Based Targets initiative (SBTi)

Institutions reporting with the SBTi’s Sectoral Decarbonization Approach (SDA) need to measure their financed emissions to create a baseline for their targets. The PCAF Standard directly supports SBTi target-setting. Financial institutions use PCAF's GHG accounting methods as the foundation for establishing science-based emission reduction targets and aligning lending and investment portfolios with the Paris Agreement's goals.

UN Principles on Responsible Investing and Banking (PRI and PRB)

The UN Principles for Responsible Investment (PRI) aims to help signatory investors understand the implications of ESG factors and incorporate them into decision-making. The UN Principles for Responsible Banking (PRB) works to ensure its signatory banks align with the UN Sustainable Development Goals and the Paris Agreement. PCAF's methodology supports both by giving investors and banks a standardized, transparent way to quantify the environmental impact of their financial activities.

Additional PCAF Principles

In addition to being built on the Greenhouse Gas Protocol framework, PCAF focuses on additional principles specifically tailored to financial institutions. These include:

1. Recognition

This principle requires financial institutions to account for financed emissions. The Standard specifically requires financial institutions to disclose using one of the following approaches for consistent reporting:

The financial control approach requires an organization to report all emissions for activities in which they can directly influence financial and operational policies and can benefit economically.

The operational control approach requires an organization to report all emissions from operations where it or one of its subsidiaries can introduce and implement operational policies.

Using these approaches ensures financed emissions are accounted for in Scope 3, Category 15. Institutions are also required to explicitly explain any information that is excluded. Information may be excluded if there’s a lack of data or if activities are small and insignificant to that institution’s total financed emissions.

2. Measurement

PCAF requires financial institutions to use PCAF methodologies to measure and disclose emissions for each asset class. Institutions must “follow the money” as far as possible to comprehend its climate impact.

PCAF requires, at minimum, the measurement of absolute emissions (the total GHG emissions of an asset class or portfolio).

When relevant, institutions can also report on emissions intensity. PCAF defines this as “absolute emissions divided by the loan and investment volume, expressed as tCO2e/€M invested.” Institutions should express emissions intensities on the sector, asset class, or portfolio level in metric tonnes of carbon dioxide equivalents per million dollars or euros invested or loaned: tCO2e/M$ or tCO2e/M€.

Institutions must also measure removed and avoided emissions if data and applicable methodologies are available. If they choose to disclose these types of emissions, PCAF requires them to report this separately from their Scope 1, 2 and 3 inventories.

Their GHG accounting measurements must:

- Align with their normal financial accounting period

- Be reported at least annually at the same point in time

- Provide an accurate representation of the reporting period emissions

- Communicate large changes that may have impacted the results

- Disclose absolute emissions for Scope 1 and 2 and relevant Scope 3 emissions in line with the GHGP’s guidance for Scope 3 emissions

- Account for emissions data at the asset class or sector level

When calculating emissions, institutions must follow these general guidelines:

- Account for the gases named in the Kyoto Protocol

- Convert gases to carbon dioxide equivalents using either GHGP’s AR5 or the IPCC’s latest assessment report

- Express in metric tonnes of carbon dioxide equivalents (tCO2e) or a suitable metric equivalent

3. Attribution

The financial institution’s emissions allocation must be proportional to the loan or investment given to the borrower or investee. This is achieved by calculating the attribution factor. Attribution factor is the share of the borrower or investee’s total annual GHG emissions that are allocated to loans or investments. It is calculated by dividing the share of the outstanding loans and investments of the financial institution by total equity and debt. Use the attribution factor to calculate financed emissions. Calculate this by multiplying the asset class’s specific attribution factor by the borrower or investee’s emissions.

How to approach PCAF financed emission calculations

Consider double-counting, data quality, and disclosure.

The PCAF Standard applies the same attribution principles for all asset classes. It’s crucial for financial institutions to follow this method so they can have one common denominator for all asset classes, consider equity and debt equally important in calculations, and avoid double-counting.

Double-counting

Double-counting is especially important to keep an eye on for institutions with both debt and equity in the same project or company. PCAF encourages institutions to minimize double-counting as much as possible.

These are the five levels at which PCAF says double counting can occur:

- Between financial institutions

- By simultaneously financing the same entity or activity

- Between transactions in the same financial institutions

- Across different asset classes

- In the same asset class

Double-counting happens when reporters count emissions more than once when calculating their financed emissions for one or more institutions. It can also occur when an institution makes loans or investments in the same value chain. PCAF recommends separately reporting Scope 1, Scope 2, and Scope 3 emissions from these financed emissions, and using the correct attribution rules to avoid double-counting.

Data quality

Financial institutions must also use the highest-quality data available for disclosures and make gradual plans to improve data quality. This helps ensure that emissions are accurately reflected and useful for decision-makers. However, PCAF recognizes that high-quality data can be difficult to come by, especially when it comes from investees or borrowers. When data is incomplete or unavailable, institutions can use proxy data to fill in the gaps.

Reporters may also need to use data collected in different years. For example, institutions may need to use their 2025 financial data and their 2024 emissions data together if this is the latest available information.

PCAF's data quality scoring system is designed to help institutions understand the reliability of their calculations and identify data gaps. Data scores also give stakeholders a way to compare disclosures. The data quality score ranges from 1 to 5, where 1 represents the highest quality data (i.e., verified, reported emissions) and 5 represents the lowest, reflecting highly estimated figures based on sectoral or regional averages.

Disclosure

Publicly disclosing findings is critical so institutions can see how their financed emissions compare with peers and how they’re contributing to the Paris Climate Agreement’s goals. Transparency also helps the financial sector as a whole get a clear view of its financial impact. PCAF’s requirements, recommendations, and methodologies all help ensure that a financial institution's disclosures are comparable and decision-useful. Disclosures should be accessible both online and through other publicly available sources.

PCAF Financed Emissions Disclosure Checklist

PCAF provides a comprehensive checklist to help financial institutions calculate financed emissions. It includes the following elements:

Reporting Requirements

General Disclosure Criteria

- Are you using either the financial control or operational control consolidation approach as outlined in the GHG Protocol Scope 3 Standard?

Coverage

- Have you included absolute financed emissions for all relevant asset classes, with justification for any exclusions?

- Have you disclosed the percentage of total loans and investments covered in your financed emissions inventory?

Absolute Emissions

- Have you disclosed absolute financed Scope 1 and 2 emissions across your loans and investments?

- Have you disclosed absolute Scope 3 financed emissions, including mandatory sectors where required?

- Have you disaggregated absolute financed emissions at the asset class or sector level?

- Have you disaggregated emissions at the sector level for the most emission-intensive sectors (e.g., energy, power, cement, steel, automotive)?

Avoided Emissions and Emission Removals

- Are avoided emissions and emission removals reported separately from your Scope 1, 2, and 3 inventories?

- Are avoided emissions reported without netting against carbon credits?

Recalculation and Significance Threshold

- Do you have a baseline recalculation protocol defining when recalculation of base year financed emissions is necessary?

- Have you established and disclosed the significance threshold that triggers base year recalculations?

Reporting Recommendations

Emission Intensity

- Have you expressed economic emission intensities at the portfolio, asset class, or sector level in tCO2e per million invested or loaned?

Data and Data Quality

- Have you reported a weighted data quality score by outstanding amount for reported emissions?

- Have you reported the weighted data quality score for Scope 3 financed emissions separately from Scopes 1 and 2?

Why should financial institutions join PCAF?

PCAF provides support and guidance with calculating and mitigating emissions.

Joining PCAF and following the PCAF Standard helps financial institutions measure and disclose the climate impact of their financed emissions. Guidance ranges from help with data collection to advice for presenting results. As a member of PCAF, organizations can get the help they need to mitigate emissions. Joining also requires a commitment to reducing emissions, which brings potential reputational benefits.

How can financial institutions join PCAF?

Follow PCAF's roadmap to join.

Institutions can join PCAF by sending a commitment letter, joining a local regional implementation team, and assessing and disclosing financed emissions.

PCAF uses this process for any financial institution that can commit to disclosing financed emissions within three years of submitting its letter. However, it’s up to the financial institution to decide the breadth of its first PCAF disclosure. For example, they can choose to disclose one asset class or a percentage of their portfolio. PCAF allows this flexibility, since data quality and availability vary greatly between institutions. There’s no fee for joining PCAF or for using its methodologies, but access to PCAF’s emission factor database and its related methodologies is reserved exclusively for PCAF signatories. After submitting a letter, financial institutions are listed on PCAF’s “financial institutions taking action” page with “committed” status. The status changes to “disclosed” after the institution has disclosed financed emissions. Those reports are also available to download on this page.

What’s next for PCAF?

The December 2025 PCAF Standard update marked a significant milestone for PCAF, but it is just one step in an ongoing process. In the months and years to come, the organization will focus on inclusive growth, improved data availability, expanded disclosure support, and continued development of the PCAF Standard—all with the goal of meeting the financial industry's needs for reliable, decision-useful emissions reporting.

Learn more about how Persefoni can support your organization with financed emissions calculations.