The UK's Streamlined Energy and Carbon Reporting (SECR) framework requires certain quoted companies, large unquoted companies, and LLPs to report energy and carbon data. The framework was designed to support the UK's overall climate strategy by improving transparency and accountability.

As the UK works towards its national goal of achieving net zero emissions by 2050, reducing energy consumption across the economy has become a central policy priority. In response, the government has introduced a range of interventions aimed at improving corporate transparency and driving decarbonization, including the Streamlined Energy and Carbon Reporting (SECR) framework.

SECR requires in-scope organizations to disclose their energy use, carbon emissions, and decarbonization efforts, with the intention of improving accountability, informing stakeholders, and encouraging energy efficiency.

Below, we take a closer look at SECR, its implementation, and how companies can prepare for reporting.

What is SECR? Why was it introduced?

The policy supports the UK’s climate strategy by requiring energy and emissions disclosure.

In April of 2019, the UK government (“HM Government”) introduced the SECR framework, which requires in-scope companies to collect and report information on their energy consumption and carbon emissions, along with efforts to improve energy efficiency and manage carbon.

The framework replaced the previous CRC Energy Efficiency Scheme and aimed to simplify requirements, reduce administrative burdens, increase transparency, and expand reporting to more companies. The SECR is part of a larger constellation of decarbonization policies and frameworks designed to support the UK’s overall climate strategy. These include the Energy Savings Opportunity Scheme (ESOS), Emissions Trading Scheme (ETS), Climate Change Levy (CCL), Climate Change Agreements (CCAs), TCFD recommendations, and, most recently, UK’s adoption of Sustainability Reporting Standards in alignment with the International Sustainability Standards Board (ISSB).

Who needs to report under SECR?

Quoted companies, large unquoted companies, and large LLPs must report.

SECR requires the following companies to submit disclosures:

- All quoted companies of any size

- Large unquoted companies incorporated in the UK (including charitable companies)

- Large limited liability partnerships (LLPs)

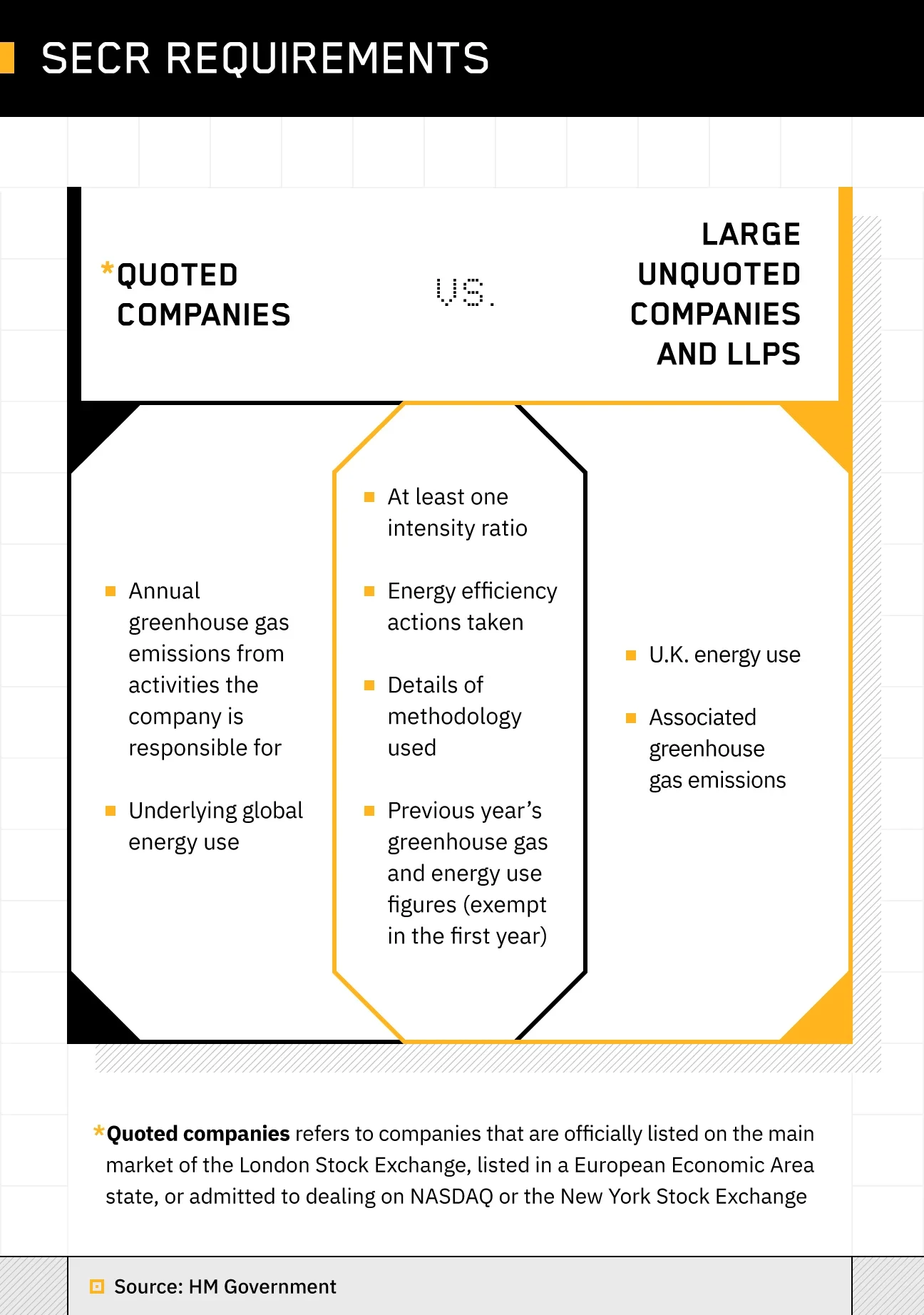

A “quoted company” is one that’s officially listed on the main market of the London Stock Exchange, listed in a European Economic Area state, or admitted to dealing on NASDAQ or the New York Stock Exchange.

Sections 465 and 466 of the 2006 Companies Act define “large” companies as those that meet at least two of the following criteria:

- A turnover of at least £36M

- A balance sheet of at least £18M

- At least 250 employees

The following organizations are exempt from SECR disclosure requirements:

- Low energy users

- Public bodies

- Organizations incorporated outside of the UK

- Private sector organizations

“Low energy users” are entities that use 40 megawatt hours or less over the financial year—roughly equivalent to the amount of energy consumed by about 14 British homes in a year.

SECR also exempts entities that are considered public bodies. Some organizations or parts of organizations may need to submit reports even if they are doing public or not-for-profit activities. These entities should verify whether or not they meet exemption requirements. Private sector organizations and entities incorporated outside of the UK are also exempt. However, exempt entities are encouraged to voluntarily participate in managing their energy efficiency and supporting the UK’s nationwide efforts.

What does SECR require companies to report?

Reports cover energy use, emissions, methodologies, and efficiency efforts.

The SECR requires companies to provide information on their energy usage and emissions, as well as the calculation methodologies used to arrive at these numbers. Companies must also describe efforts they’ve undertaken to improve energy efficiency, and provide a year-over-year comparison. Below is a broad overview of the information required for SECR reports.

- Energy use, including gas, purchased electricity, and transport fuel

- GHG emissions reported in tons of carbon dioxide equivalent (CO2e)

- Methodology used to make calculations for emissions and energy use

- At least one intensity ratio comparing emissions to a business metric

- A narrative description of efforts taken to improve the company’s energy efficiency during the financial year

- Previous years’ figures for GHG emissions and energy use

Businesses need to start by identifying their boundaries and which parts of the business they must report on. This is especially relevant for companies with complex structures. Reporting organizations can use the following boundaries:

- Financial control boundary: A company reports on all sources of environmental impact that it has financial control over

- Operational control boundary: A company reports on all sources of environmental impact that it has operational control over

- Equity share boundary: A company accounts for GHG emissions from operations based on its equity in the operation

The Climate Disclosure Standards Board (CDSB) Framework aligns environmental and social information with the boundaries used for financial reporting.

The Financial Reporting Council (FRC) created the 2019 SECR taxonomy to reflect the SECR reporting requirements. This update allows companies to tag SECR data and improve transparency and accessibility. Additionally, HM Government stipulates that disclosures must be accessible and easily understood by stakeholders. Some SECR requirements are determined based on the type of reporting organization — we’ll go over these differences in the next section.

Omitted information

In some cases, the SECR allows companies to omit information. However, companies are required to include an explanation for omitted information, and they may be questioned by the Financial Reporting Council as a result of omitted information. Companies may omit information when:

- Disclosing the information would be seriously prejudicial to the organization’s interest. This reasoning should be used under exceptional circumstances, like an acquisition or restructuring.

- Energy and carbon information are not practical to obtain. SECR recommends also including the materiality of the information and the actions the company is taking to obtain that information.

Voluntary information and actions

Guidance from HM Government includes recommendations for additional voluntary information and actions for more robust reporting. Below are some examples of these recommendations.

- Alignment with Task Force on Climate-related Financial Disclosures (TCFD) recommendations for reporting forward-looking financial risks and opportunities resulting from climate change

- External verification/assurance to review the consistency, completeness, and accuracy of the information in the disclosure

- Reporting scope 3 emissions or specific scope 3 emissions (depending on the type of organization)

- Setting forward-looking science-based emissions reduction targets that go beyond requirements to report on the current and previous financial year

- Determining the materiality of emissions to gain a better understanding of the business's impact on the environment

HM Government includes these and more recommendations to provide companies with best practices to follow. These additions can enhance reports and provide stakeholders with more extensive information useful for decision-making.

How do SECR requirements differ between types of organizations?

Categories of companies face different reporting obligations.

The SECR disclosure requirements for energy usage and GHG emissions differ between quoted companies, large unquoted companies, and LLPs. Here’s a look at what each category must disclose:

Quoted Companies

- Annual global emissions from activities the company is responsible for, including combustion of fuel and the operation of any facilities (also known as scope 1 emissions)

- Annual emissions from the purchase of heat, steam, cooling, or electricity by the company for its own use (also known as scope 2 emissions)

- Methodologies used in calculations

- At least one intensity ratio

- Previous year’s figures for GHG emissions and energy use

- Underlying global energy consumption used to calculate GHG emissions in kWh, including the previous year’s figure

- Information about energy efficiency action taken during the organization’s financial year

- Proportion of the company’s energy consumption and emissions related to emissions and energy consumption in the UK (including offshore area)

When reporting on GHG emissions, quoted companies must ensure that the GHG accounting approach used covers the required emissions activities they are responsible for and must report on.

Emissions reports must also align with the requirements for the Directors’ Report. HM Government states a strong preference for energy and carbon reports that align with the boundaries of financial statements.

Quoted companies must report on emissions from the following GHGs:

- Carbon dioxide (CO2)

- Methane (CH4)

- Nitrous oxide (N2O)

- Hydrofluorocarbons (HFCs)

- Perfluorocarbons (PFCs)

- Sulfur hexafluoride (SF6)

Companies are encouraged to consider reporting on nitrogen trifluoride (NF3), especially if it is material to the company.

They must also make clear if reporting emissions from activities they are responsible for results in either of the following scenarios:

- Reporting on energy use and GHG emissions from operations not included in their statements

- Not reporting on energy use and GHG emissions from certain operations covered by the consolidated financial statement

Explanations of omitted or additional inclusions of emissions data should be clear and include if and how the information differs from operations within the consolidated financial statement.

Large unquoted companies incorporated in the UK and LLPs

Disclosures from large unquoted companies and LLPs include UK energy use and associated GHG emissions. Offshore undertakings must disclose energy use and emissions for the UK and offshore areas. Below is a summary of requirements for large unquoted companies incorporated in the UK and LLPs.

- UK energy use, including purchased electricity, gas, and transport

- Associated GHG emissions in CO2e as a result of the total UK energy use

- Methodologies used in calculations

- At least one intensity ratio

- Previous year’s figures for GHG emissions and energy use

- Information about energy efficiency action taken during the organization’s financial year

At a minimum, these companies must report these figures related to the annual quantity of energy:

- Consumed in the UK, resulting from the purchase of electricity by the company for its own use, including transportation

- From stationary or mobile activities involving the combustion of gas that the business is responsible for

- From transportation, where the organization is responsible for purchasing fuel for business purposes

These companies can also voluntarily report information, especially if it significantly affects their emissions or energy. Some examples include:

- Unconsumed energy that the organization does not use or supplies to a third party

- Energy consumed outside the UK (unless the business is an offshore undertaking)

- Fuel associated with train travel by a company’s employees, where the company does not operate the train

- Fuel associated with the transportation of goods, where the business subcontracts a firm or self-employed individual to undertake the work for the business

How can businesses improve SECR reporting and compliance?

5 steps to prepare for reporting

Compliance with SECR demands reliable, auditable emissions and energy data. Companies can build confidence in their reporting by taking the following steps:

- Clarify scope and organizational boundaries. Determine whether your organization is required to report under SECR, and identify which entities and activities you need to report on. Getting clear on boundaries and scope early on will prevent inconsistency and errors later in the reporting process.

- Build a cross-functional team. Assign clear responsibility for SECR reporting, involving finance, sustainability, and operations teams as needed. Senior-level oversight helps ensure accuracy, completeness, and alignment with broader business strategy and statutory reporting obligations.

- Establish reliable systems for data collection. You’ll need repeatable processes for capturing data on energy consumption and emissions from electricity, transportation, and other sources. Gathering data is often the most time-consuming step—you can find tips here for streamlining the process.

- Calculate emissions using recognized methodologies. Utilizing an SECR-aligned carbon accounting platform will help ensure methodologies and emissions factors are consistent and calculations are documented and audit-ready.

- Identify and document energy efficiency actions. Review energy data to identify opportunities for reducing consumption and emissions, and document existing or planned efficiency measures.

Preparing for SECR can deliver benefits beyond regulatory compliance. By systematically tracking energy use and emissions, SECR encourages companies to develop a clear understanding of their operational efficiency, decarbonization pathways, and climate risks and opportunities —ultimately strengthening resilience. Reporting also helps companies respond to increasing scrutiny from investors, customers, and other stakeholders. Organizations that use SECR as a strategic tool rather than a reporting exercise will build a foundation for long-term value creation and competitiveness in a low-carbon future.

Learn more about Persefoni’s all-in-one carbon accounting platform and how your business can use it to prepare for SECR reporting.

SECR FAQs

How is SECR enforced?

The Conduct Committee of the FRC is responsible for monitoring compliance for both reports and relevant accounts based on requirements from Part 15 of the Companies Act 2006. The committee can:

- Launch investigations if they determine companies have not provided relevant disclosures

- Apply for a declaration that annual reports or accounts don’t comply with requirements and, as a result, require a revised report and/or set of accounts

Companies House cannot accept accounts for companies and LLPs that don’t meet the requirements of the Companies Act 2006. Companies that submit reports after the filing deadline are liable for civil penalties and any action taken against directors or LLP members.

When was SECR introduced?

SECR was first introduced in April 2018 when the Companies (Directors’ Report) and Limited Liability Partnerships (Energy and Carbon Report) Regulations 2018 came into force.

What is the difference between SECR and UK’s Sustainability Reporting Standards (SRSs)?

SECR is a current mandatory reporting requirement for energy and carbon disclosures, whereas UK’s Sustainability Reporting Standards (SRSs) are a set of new, broader, IFRS-aligned standards that will include a wider range of sustainability information and provide a unified framework for sustainability-related financial reporting.

What is the difference between ESOS and SECR?

ESOS audits only energy consumption rather than energy and GHG emissions like SECR. ESOS also includes different scopes of businesses that are mandated to comply.

ESOS is the UK energy assessment scheme introduced in 2014 to improve energy efficiency in the UK Qualifying businesses must submit information on total energy consumption, energy efficiency, and energy savings opportunities.

Where do businesses include SECR disclosure information?

SECR disclosures must be included in the company’s Directors’ Report or similar energy and carbon report. These must be filed with Companies House. LLPs will need to file a separate energy and company report and submit it to Companies House.

Businesses can also include SECR disclosure information in strategic reports if SECR is embedded in a company’s strategy. However, companies must explain this decision in the Directors’ Report.

How does subsidiary and group-level reporting work?

Group-level reporting includes disclosures for parent companies and their subsidiaries. This can affect how parent and subsidiary companies submit their disclosures.

For example, subsidiaries must take into account energy usage from their parent company and subsidiaries (if included in a group report) to seek an exemption. Subsidiaries may not be required to include SECR disclosure information in their reports if it is already included in a group-level report.

Parent companies can omit a subsidiary’s information if SECR doesn’t require the subsidiary to report if it were disclosed independently.