Methodologies for Calculating Scope 3 Emissions

Updated:

January 13, 2026

·

[Read Time]

Regardless of whether an organization is in the crawl, walk, or run stage of its carbon accounting journey, calculation methods and emission factors play a central role in determining the accuracy and usefulness of Scope 3 emissions data.

Calculation methodologies refer to the techniques used to convert business activity data—such as spend, distance, fuel use, or quantities purchased—into greenhouse gas (GHG) emissions. These methods are primarily defined by the GHG Protocol, with additional, category-specific guidance provided by initiatives such as the Partnership for Carbon Accounting Financials (PCAF) for financed emissions.

Scope 3 emissions are organized into 15 categories, each representing a different type of upstream or downstream activity. Because these activities vary significantly in how emissions are generated, there is no single calculation method that applies across all categories.

For example:

Common calculation approaches include:

These approaches are often used early on because distance or spend data is commonly available.

Calculation methods depend on how products generate emissions during use, such as:

These methods focus on how products are used over their lifetime rather than how they are manufactured.

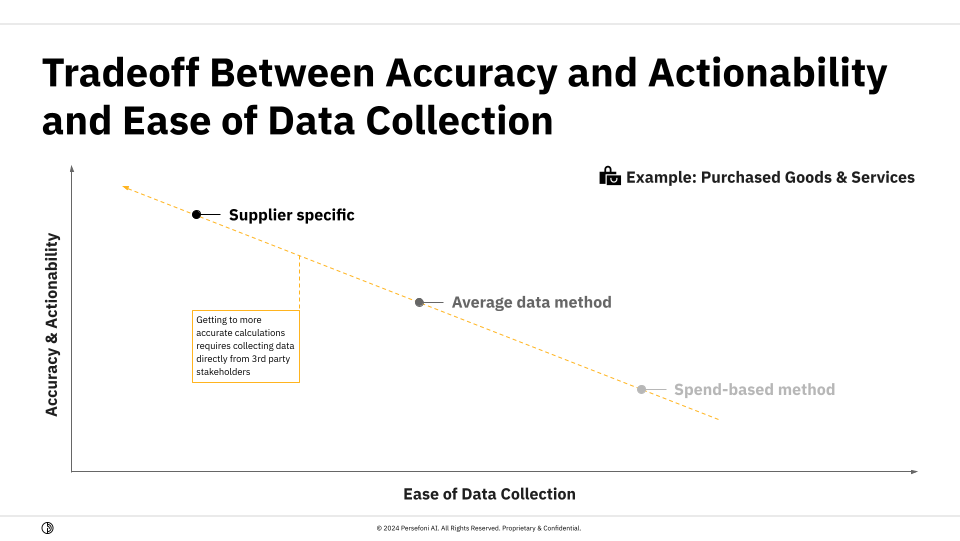

Many Scope 3 categories allow for multiple acceptable calculation methods. For example, Purchased Goods and Services (Scope 3: Category 1) can be calculated using:

Each approach has tradeoffs:

When selecting a calculation methodology, organizations should consider:

All of these methods are considered acceptable under the GHG Protocol when applied appropriately. The goal is not to choose the “perfect” method immediately, but to start with feasible approaches and improve data quality and granularity over time as Scope 3 programs mature.

Scope 3 calculation methodologies are designed to be flexible. By selecting methods that align with available data and business priorities, and improving those methods over time, organizations can build Scope 3 inventories that are both practical and decision-useful.