SB 253 GHG Accounting and Assurance

Updated:

January 7, 2026

·

[Read Time]

Now that we’ve established a high-level understanding of California’s climate disclosure laws, this lesson takes a closer look at what SB 253 requires from a greenhouse gas accounting and assurance perspective.

In this lesson, we’ll focus specifically on:

This lesson builds directly on the overview from Lesson 1 and sets the foundation for understanding how SB 253 works in practice.

Under California’s Climate Corporate Data Accountability Act (SB 253), in-scope companies must prepare and publicly disclose annual greenhouse gas (GHG) emissions through the California Air Resources Board (CARB) in accordance with the GHG Protocol Corporate Accounting and Reporting Standard and related guidance.

SB 253 applies to U.S. companies (public and private) that are “doing business in California” and have total annual revenues exceeding $1 billion, subject to certain statutory and proposed exemptions.

CARB’s proposed rulemaking would require covered entities to report their full GHG emissions inventory globally, not just emissions within California, on an annual basis.

CARB’s initial rulemaking proposals and draft guidance provide specific deadlines and phased expectations:

CARB staff stated that SB 253 requires Scope 1 and Scope 2 greenhouse gas emissions reporting beginning in 2026, with a first-year–only reporting deadline established through initial regulation. Based on stakeholder feedback, CARB staff proposed a first-year Scope 1 and Scope 2 reporting deadline of August 10, 2026.

CARB further specified how the reporting period is determined for fiscal-year reporters:

CARB also clarified several points intended to support first-year compliance:

CARB emphasized that it would exercise enforcement discretion for good-faith first-year submissions, with the goal of supporting entities actively working toward compliance.

Scope 3 reporting is expected to be phased in beginning in 2027, covering the entity’s 2026 data. While precise reporting deadlines and templates for Scope 3 have not yet been finalized, CARB’s rulemaking anticipates adding these requirements as part of subsequent regulatory updates.

CARB’s rulemaking is ongoing, and additional reporting templates, content requirements, and compliance details (including enforcement timelines) are expected to be finalized through formal regulation later in the rulemaking process.

Entities subject to SB 253 must make their GHG reports publicly accessible, typically by submitting them to a CARB public docket with a link to the report included in CARB’s reporting system.

SB 253 establishes a phased approach to third-party assurance of emissions disclosures, recognizing that many companies are still maturing their GHG data, systems, and controls. The statute initially requires limited assurance (final timing to be determined), with a planned transition to reasonable assurance for certain emissions over time.

Limited assurance represents a lower level of confidence than what companies are accustomed to for audited financial statements. Under limited assurance, the assurance provider performs primarily inquiry- and analytics-based procedures and issues a negative assurance conclusion, stating that nothing has come to their attention that would cause them to believe the disclosed emissions contain a material misstatement.

This contrasts with reasonable assurance, which involves more extensive testing and results in a positive opinion that the disclosures are fairly stated in all material respects.

SB 253 requires Scope 1 and Scope 2 emissions to progress from limited assurance to reasonable assurance on a defined timeline, reflecting regulators’ expectations that these emissions are generally more controllable and measurable. Scope 3 emissions, which are inherently more complex and dependent on supplier and value-chain data, are introduced later and remain subject to limited assurance for a longer period under the statute.

Importantly, this phased approach underscores the need for companies to begin strengthening their emissions data foundations now—by improving data quality, documentation, audit trails, and internal controls—so they are prepared not only to meet initial limited assurance requirements, but to withstand the higher scrutiny of reasonable assurance in the years ahead.

During a limited assurance engagement, the assurance provider performs a set of targeted, risk-based procedures designed to evaluate the credibility and completeness of a company’s GHG emissions inventory. The objective is not to provide absolute certainty, but to assess whether the disclosed emissions data has been prepared in accordance with applicable standards and is free from material misstatement.

Companies should expect assurance providers to perform procedures that commonly include:

Importantly, a limited assurance engagement is not intended to re-audit every data point or replicate the company’s emissions inventory. Instead, the focus is on whether the inventory, taken as a whole, has been prepared in a manner that is reasonable, consistently applied, and aligned with recognized frameworks such as the GHG Protocol.

As a result, companies with well-documented methodologies, transparent assumptions, and traceable data are significantly better positioned to move through limited assurance efficiently, and to build a strong foundation for future reasonable assurance requirements.

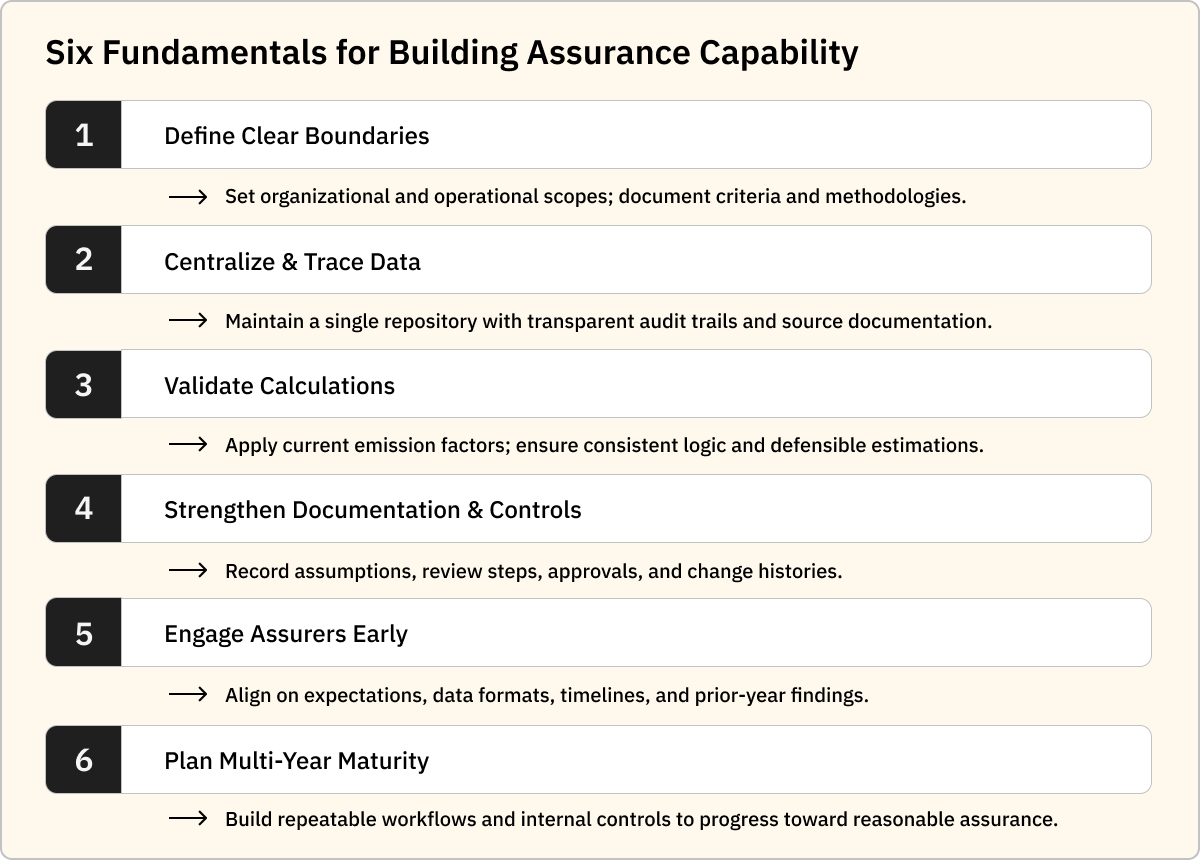

One of the most important readiness tools for assurance under SB 253 is an inventory management plan.

An inventory management plan documents the “story” of how a company’s greenhouse gas inventory was developed. This includes decisions made throughout the process, from defining organizational boundaries to selecting calculation methodologies.

A strong inventory management plan typically explains:

Documenting this information as emissions are calculated, rather than retroactively, can significantly streamline the assurance process and reduce friction with auditors.

In addition to documenting emissions calculations, companies are encouraged to engage with their assurance providers early. SB 253 assurance is not a one-week exercise; companies should plan for a multi-month process from initial engagement through final sign-off.

As a general expectation, companies should anticipate at least two months for the end-to-end Scope 1 and Scope 2 assurance process. This includes time for document requests, sample testing, clarification questions, and final reporting.

Many companies are also choosing to run a “test” assurance engagement ahead of their first regulated filing. Rather than waiting to assure 2025 data for the 2026 reporting cycle, some companies are asking their auditors to review earlier inventories, such as 2024 emissions data. This allows teams to familiarize themselves with the assurance process, identify gaps, and refine internal controls before reporting becomes mandatory.

SB 253 requires companies not only to measure their greenhouse gas emissions, but to do so in a way that can stand up to third-party review.

Early preparation is critical. Companies that begin documenting methodologies, formalizing inventory management practices, and engaging with assurance providers ahead of their first reporting year will be better positioned to navigate SB 253 efficiently and with confidence.

In Lesson 3, we’ll shift focus from emissions data to climate-related financial risk reporting under SB 261. That lesson will cover how companies are expected to assess and disclose climate risks and opportunities, and how those disclosures align with established frameworks such as TCFD.