Overview of California Climate Disclosure Laws SB 253 and 261

Updated:

January 7, 2026

·

[Read Time]

Welcome to Persefoni Academy’s course on California climate disclosure. This course is designed to help companies understand and prepare for California’s new climate reporting requirements.

Throughout this course, we’ll walk through the structure of California’s climate disclosure laws, what they require, who they apply to, and how companies can begin preparing. This first lesson provides a high-level overview of the California Climate Accountability Package. In later lessons, we’ll take deeper dives into specific requirements under each law.

Before we begin, it’s important to note that this course is intended to be educational. Persefoni is not providing legal advice, and companies should consult their legal and compliance teams as they evaluate their obligations under California law.

California’s climate disclosure requirements are established through two pieces of legislation: SB 253 and SB 261. Together, these laws are designed to improve transparency around corporate greenhouse gas emissions and climate-related financial risks, providing clearer information to investors, consumers, and other stakeholders.

These laws build on California’s long history of climate policy and greenhouse gas regulation. The California Air Resources Board (CARB) has administered mandatory greenhouse gas reporting programs for decades, and these climate disclosure laws extend that experience to a broader set of companies operating in the state

While the two laws are closely related, they address different types of disclosures and have different thresholds and timelines. Understanding how they fit together is an important first step.

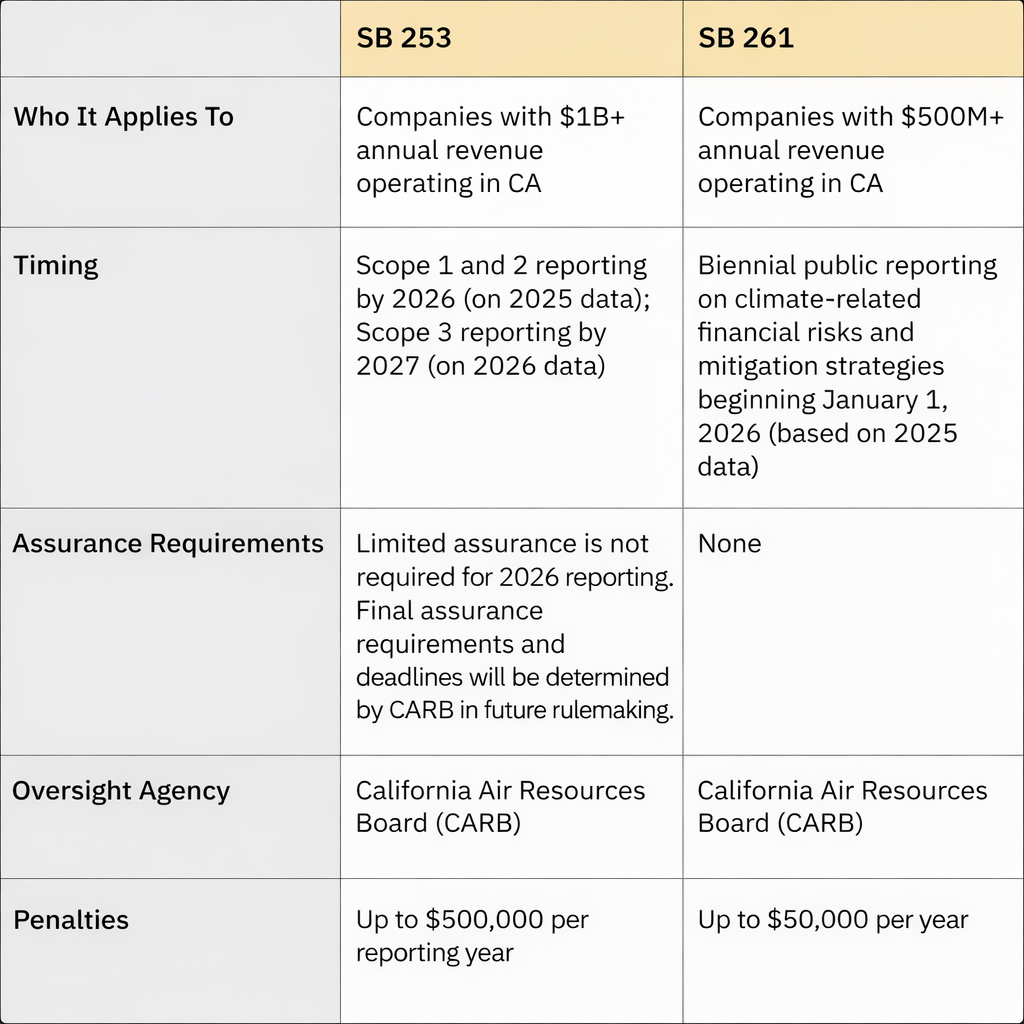

SB 253 establishes a requirement for certain companies to publicly disclose their greenhouse gas emissions on an annual basis. The law applies to U.S.-based entities that are doing business in California and exceed a specified revenue threshold.

At a high level, SB 253 requires reporting of:

The law specifies that emissions must be calculated using methodologies aligned with the Greenhouse Gas Protocol, a globally recognized standard. SB 253 also establishes a phased approach to third-party assurance, with assurance requirements becoming more robust over time.

We’ll explore the details of emissions accounting, organizational boundaries, assurance timelines, and reporting mechanics in Lesson 2.

SB 261 focuses on climate-related financial risk rather than emissions data. It requires certain companies to prepare and publicly disclose a climate-related financial risk report every two years.

These reports are intended to describe:

SB 261 is aligned with established climate risk disclosure frameworks, particularly the Task Force on Climate-Related Financial Disclosures (TCFD), as well as equivalent frameworks such as ISSB’s IFRS S2. Companies are expected to structure their disclosures around governance, strategy, risk management, and metrics and targets.

We’ll take a deeper look at climate risk reporting requirements and practical considerations in Lesson 3.

Both SB 253 and SB 261 apply only to U.S.-based entities that are doing business in California and exceed certain revenue thresholds. The thresholds differ between the two laws.

At a high level:

CARB has proposed defining revenue based on gross receipts, using existing California tax definitions. Applicability is assessed at the entity level, and companies are responsible for determining whether they meet the criteria based on their own facts and circumstances

CARB has also proposed using an established definition of “doing business in California” based on economic nexus, rather than physical presence alone. We’ll revisit these definitions in more detail later in the course.

Although the statutes establish core requirements, CARB is responsible for developing the implementing regulations that determine how reporting works in practice. This includes setting reporting deadlines, defining terms, establishing fee structures, and clarifying expectations.

CARB has been engaging stakeholders through a series of public workshops and has released draft templates, FAQs, and checklists to support early understanding and compliance. Importantly, CARB has emphasized a supportive, good-faith approach as the programs launch, particularly in the first reporting years

At a high level:

Specific deadlines and mechanics will continue to be refined through CARB’s rulemaking process, which is ongoing.

While SB 253 and SB 261 address different types of disclosures, they are designed to be complementary.

SB 253 focuses on measuring and disclosing emissions, providing quantitative data about a company’s greenhouse gas footprint. SB 261 focuses on understanding and disclosing climate-related risks, providing qualitative and strategic context about how climate change may affect a company’s financial performance.

Together, these disclosures are intended to give stakeholders a more complete picture of a company’s climate exposure and preparedness.

This introductory lesson provides the context needed to understand California’s climate disclosure requirements at a high level. In the next lessons, we’ll move from overview to application.

In Lesson 2, we’ll take a closer look at SB 253 greenhouse gas accounting and assurance. In Lesson 3, we’ll focus on SB 261 climate-related financial risk reporting. Finally, we’ll step back to discuss how companies can build a practical, phased approach to California readiness over time.