Importance of Scope 3 Emissions

Updated:

January 13, 2026

·

[Read Time]

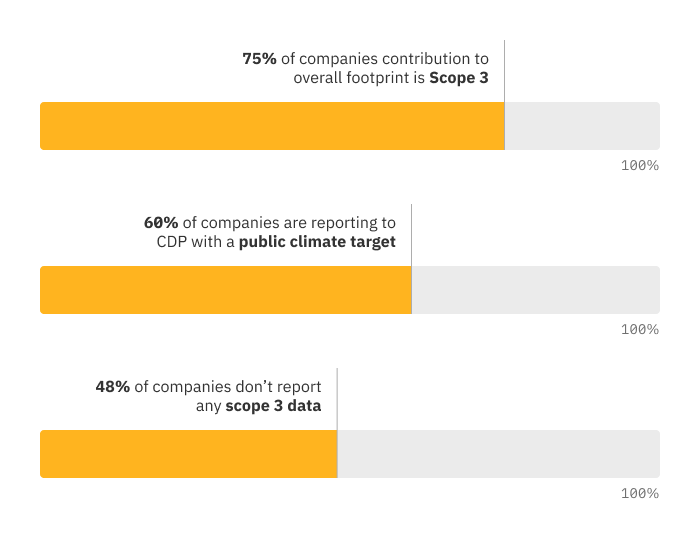

For most organizations, Scope 3 emissions represent the largest share of total greenhouse gas (GHG) emissions, often accounting for the majority of climate impact across the value chain. These emissions occur upstream and downstream of a company’s direct operations and include activities such as purchased goods and services, transportation, product use, and investments.

Because of their scale, excluding Scope 3 emissions from a greenhouse gas inventory typically results in a materially incomplete view of an organization’s climate impact. Without visibility into value-chain emissions, organizations are limited in their ability to identify meaningful reduction opportunities and develop effective decarbonization strategies.

Despite their significance, Scope 3 emissions remain underreported. According to CDP’s 2023 climate disclosure data, only 41% of more than 23,000 disclosing organizations reported at least one Scope 3 emissions category. This gap persists even as corporate climate commitments continue to increase.

As a result, a substantial portion of corporate climate impact remains unmeasured and undisclosed, even when Scope 3 emissions are likely to be material. In many cases, organizations publicly disclose climate targets without reporting the full value-chain emissions needed to assess progress toward those targets.

Expectations around Scope 3 emissions are rising as reporting frameworks, disclosure platforms, and target-setting initiatives converge:

Together, these developments signal that Scope 3 emissions are no longer optional or supplementary. They are becoming a critical input to credible climate reporting, target-setting, and transition planning.

Failing to measure Scope 3 emissions can introduce several risks:

Measuring Scope 3 emissions is essential for understanding an organization’s full climate impact, meeting evolving disclosure and target-setting expectations, and supporting informed, decision-useful climate strategies. As standards and regulations continue to mature, Scope 3 emissions are becoming a foundational element of credible corporate climate action.