As climate-related disclosures gain momentum, companies are facing rising expectations for credible greenhouse-gas (GHG) emissions reporting. And with that, the shift toward third-party, independent assurance. This isn’t just about checking boxes: assurance provides independent confirmation that your emissions data is complete, traceable, and aligned with your selected standard. It strengthens your credibility with investors, regulators, supply chains, and ultimately supports strategic decarbonization.

For many organizations, assurance remains a newer terrain: unfamiliar audit language, new data demands, and new internal controls. To streamline assurance readiness and reduce risk, it helps to approach assurance preparation not as a one-time activity, but as a maturity journey.

This article outlines a step-by-step roadmap, illustrating what good preparation looks like, how to structure your program, and how to build the capability to move from limited to reasonable assurance.

What Assurance Means in GHG Reporting

In sustainability, “assurance” refers to a formal, independent review of the subject matter (e.g., your emissions inventory) by a qualified party. The reviewer’s goal is to provide a written conclusion on whether the subject matter is prepared, in all material respects, in accordance with the criteria you have applied.

Some key distinctions to understand:

- Level of assurance:

- Limited assurance (akin to a review engagement) provides a moderate level of confidence. The practitioner performs inquiry and analytical procedures, requiring less extensive evidence.

- Reasonable assurance (akin to an examination engagement) provides a higher degree of confidence. It requires more rigorous procedures, including testing internal controls, validating source documents, and assessing risks of material misstatement. AICPA attestation standards outline the specific differences between these levels.

- Subject matter and criteria:

Your emissions inventory is the subject matter; the criteria are your selected standard (e.g., the GHG Protocol Corporate Standard, Scope 2 Guidance, Scope 3 Standard). For example, the GHG Protocol provides transparency and structure for Scope 1, 2, and 3 classification. - Assurance providers & standards:

Assurance over GHG emissions can follow international standards such as ISAE 3410 (Assurance Engagements on Greenhouse-Gas Statements) or national attestation standards (e.g., AICPA AT-C sections).

Why It Matters

Beyond satisfying stakeholder demands, assurance readiness reflects process maturity: traceability, control, and governance. It reduces exposure to reputational or regulatory risks. It also helps organizations leverage their reporting program as a management asset, not just a compliance output.

A Six-Step Roadmap to Assurance Readiness

The transition to effective assurance begins with foundational capabilities. While each organization’s journey will differ, companies that perform well in the assurance review often share a similar set of attributes:

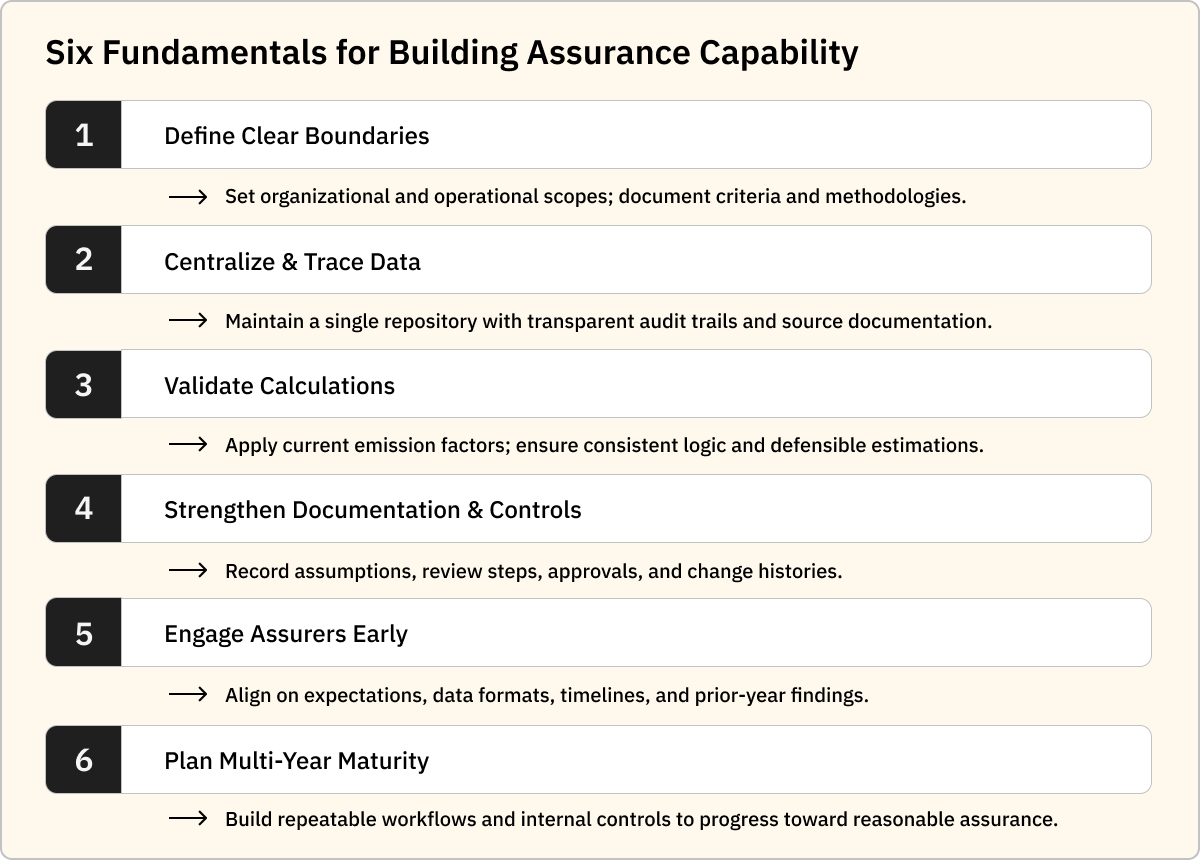

1. Set a Clear Boundary & Methodology Framework

Before data gathering begins, your company must define the following:

- Organizational boundary: Which entities, business units, or legal structures are included? Are you using control, equity, or operational consolidation?

- Operational boundary and scope definitions: Which emissions types do you capture (Scope 1, Scope 2, Scope 3)? Are leased assets included, business travel, etc.?

- Methodology documentation: For each emissions category you adopt or estimate, document the methodology, emission factors, assumptions, exclusions, and how boundary decisions were made. This is often referenced by auditors as a “starting point”.

- Criteria for estimation and exclusions: Where estimations or exclusions occur, the rationale must be documented and defensible.

Companies that struggle in assurance reviews often have weak or incomplete boundary/methodology rationales, leading to auditor queries and delays. Auditors typically start with the “bookends” of your inventory (the boundary and methodology) before drilling into calculations.

2. Build Traceable, Centralized Activity Data

Data is only helpful in assurance if it is traceable. That means having:

- Single repository: All activity data live within a controlled environment—ideally a platform or controlled spreadsheet system.

- Structured file system: Auditors appreciate consistency. Using a standardized four-file pattern across categories (raw → cleansed → upload template → final ledger) can make the auditor review far smoother.

- Source documentation tied to data points: For example, invoices, consumption reports, and meter readings should link to reported activity data with clear mapping.

- Version control and change logs: Auditors look for evidence of how data has changed, how corrections were made, and how reconciliations were performed.

- Automated checks and sense-checks: While not required, companies with automated data validation (unit conversions, anomaly detection) tend to face fewer auditor questions.

In short: if you can’t answer “Where did this number come from?” and “How was it derived?” for your largest data items, you’ll likely face auditors wanting to dig deeper.

3. Ensure Calculations & Emission Factors Are Verified

Data without correct calculations is a common risk. Key areas that frequently attract auditor findings include:

- Outdated emission factors: Using stale factors can increase misstatement risk.

- Unit conversion or inconsistent units: Mismatches between source units and report units are common audit flags.

- Mismatch between invoices/consumption and reported data: Auditors want to see that consumption aligns with bills or submeters.

- Estimation logic not documented: Estimations are acceptable, but the method must be documented, assumptions disclosed, and high-level sense checked. Estimations are not disqualifying, but unexplained estimations are.

- Consistency of methodology year-to-year: Changes in approach must be documented and rationalized.

4. Maintain Robust Documentation & Internal Control Framework

Documentation is arguably the single most differentiating factor between straightforward and problematic audits. Companies ready for assurance typically have in place:

- A formal GHG inventory management plan or methodology manual.

- Documentation for each data source: what it is, who owns it, and how often it is updated.

- Documentation of assumptions, estimations, exclusions: why they were used and who approved them.

- Internal review procedures and sign-off records: Who reviewed the data, when, and what findings were resolved.

- Audit trails: Evidence of reconciliations, adjustments, and versioning.

- Change-control logs: When the methodology changed, when data was restated, and how prior year data was handled.

When documentation is well-structured, the audit “timeline compresses” significantly, and cost participation tends to decrease. If documentation is weak, the back-and-forth multiplies, possibly turning assurance into a major project rather than a straightforward review.

Additionally, aligning your internal control environment with the framework used in financial audits (for instance, using the COSO Internal Control — Integrated Framework structure) demonstrates maturity and can reduce auditor skepticism.

5. Engage Your Assurance Provider Early

Many companies treat assurance as a final step, something that happens after the data has been compiled. That can create avoidable risk. Instead, you should:

- Start preliminary discussions 2-3 months ahead of submitting your inventory.

- Use your assurance provider as a partner in readiness, not just an auditor. Share your file structure, methodology draft, key data flows, and ask for feedback. Meeting with your auditor before a single file is ready can save you weeks of back-and-forth.

- Agree on submission formats, access methods (platform login, spreadsheets, portal), timing, and deliverables.

- Review prior-year assurance findings (if any) and ensure corrective actions are baked into your process.

- Lock in your timeline: Once the auditor begins procedures, it may take 8–12 weeks (depending on complexity and maturity) from kickoff to conclusion.

By structurally embedding auditor engagement early, you reduce surprises and ensure the assurance process is efficient rather than disruptive.

6. Build a Multi-Year Improvement Roadmap Toward Reasonable Assurance

While most companies begin with limited assurance, the trajectory increasingly points to next-stage review: reasonable assurance. To prepare for that:

- Strengthen internal controls over ESG data, just as you would with financial reporting.

- Formalize repeatable workflows: data collection, review, sign-off, and archiving.

- Enhance data architecture and auditability: systems that log changes, show lineage, and support reconciliations.

- Expand documentation of controls: who is responsible, what checks are performed, and how exceptions are handled.

- Prepare for deeper testing: reasonable assurance means auditors will sample underlying records and perform detailed testing, not just analytical review.

- Monitor evolving assurance standards and frameworks, such as the new guidance from AccountAbility on the AA1000 Assurance Standard.

Building this maturity roadmap early helps ensure your assurance ecosystem is scalable and resilient, so you’re not scrambling when deeper assurance becomes expected.

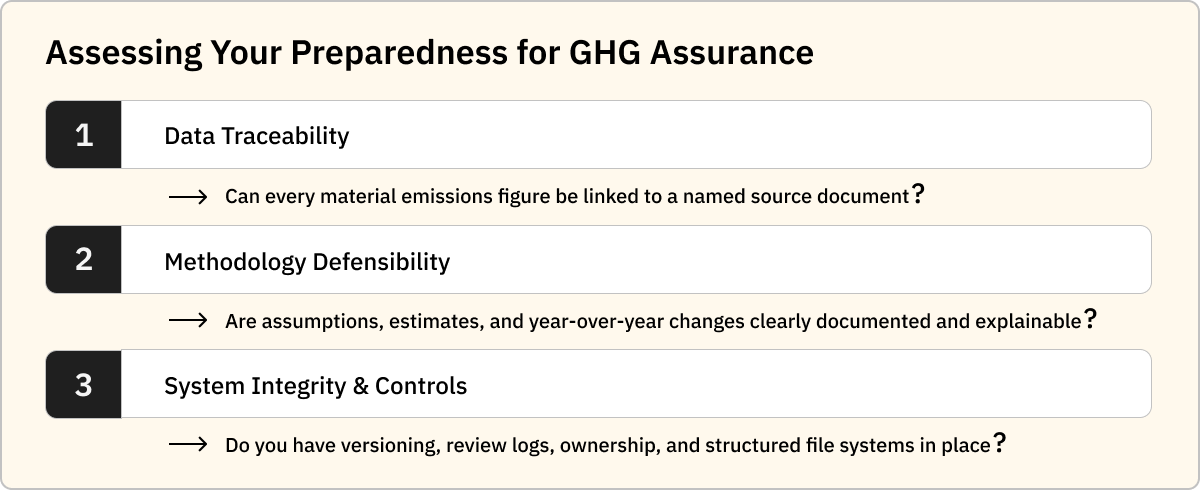

Three Questions to Gauge “Ready Enough” for Assurance

Every organization asks themselves: How do we know when we’re ready for assurance? Because perfection is neither required nor realistic, the key is defensibility.

Ask yourself:

- Can I trace each material emissions figure back to a named source document (invoice, meter reading, contract)?

- Can I explain the methodology, assumptions, and changes from the prior year, and provide supporting documentation?

- Do I have structured file systems, version control, review logs, and sign-offs that show data integrity and ownership?

If you can answer “yes” to these, you’re likely in good shape to invite an assurance provider and execute confidently. If you are still missing key documents, don’t delay. Build the missing link now rather than pivoting mid-audit.

Building a Resilient Framework for Reliable Disclosure

Assurance preparation should be treated as a strategic program. While many organizations focus on the deadline of the audit, the real work is subtle: building traceable data systems, defensible methodologies, rigorous controls, and strong documentation.

By aligning your boundary definitions, centralizing your data, verifying your calculations, documenting comprehensively, engaging early with your assurance partner, and mapping a multi-year maturity path, you can transform assurance from a “pain point” into a differentiator. A process that reflects maturity, enhances stakeholder trust, and supports your decarbonization agenda.