Bilan Carbone® is a rigorous carbon accounting methodology developed by the French government to help organizations and local government authorities accurately measure and reduce their greenhouse gas emissions. A central pillar of the approach is the use of emission factors from Base Carbone®, a public database that is managed by ADEME, France’s Environment and Energy Management Agency.

As climate disclosure and decarbonization become increasingly important strategic considerations, businesses need to be able to accurately measure their greenhouse gas emissions and compare their progress with peers. The French government designed Bilan Carbone® with this purpose in mind. Today, companies throughout France and the European Union use the methodology to produce actionable insights into their carbon footprints and comply with disclosure regulations, notably France’s BEGES reporting requirement. A core component of the Bilan Carbone® framework is Base Carbone®, a public database of emission factors used to calculate carbon footprints.

Below, we’ll answer key questions about Bilan Carbone® — what it is, why it was created, and how companies can apply it.

What is Bilan Carbone®?

The French framework supports organizations in calculating and reporting GHG emissions.

Bilan Carbone® is a carbon accounting methodology originally developed in the early 2000s by ADEME, the French public agency responsible for ecological transition. Since then, oversight of the framework has transferred to the Association Bilan Carbone® (ABC), which continues to maintain and evolve it. Bilan Carbone® (loosely translated as “carbon footprint assessment”) helps organizations quantify their total greenhouse gas emissions, including both direct and indirect emissions, with the ultimate goal of supporting effective climate transition plans.

.png)

Methodology

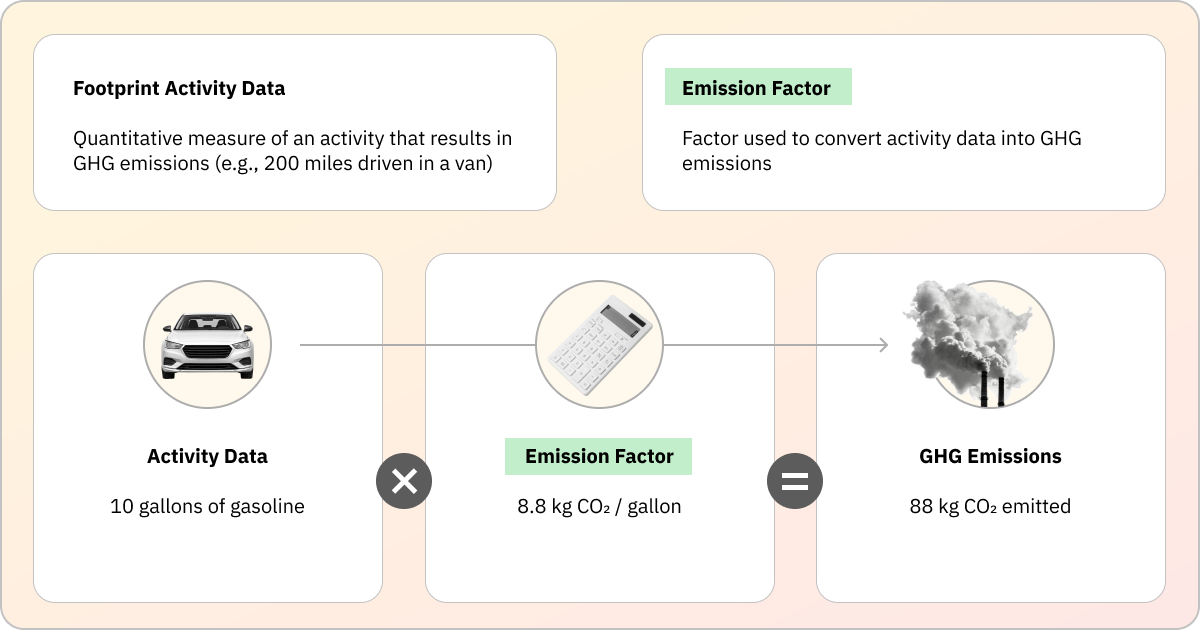

Bilan Carbone® uses a simple and widely accepted carbon accounting equation:

Emissions = Activity Data × Emission Factor

This calculation applies standardized factors to convert information about real-world activities (e.g., fuel use or kilometers traveled) into emissions estimates.

Bilan Carbone® is a rigorous approach. It emphasizes physical activity data over spend-based emissions calculations for greater accuracy. One of the defining features of the framework is its lifecycle/value chain focus—organizations applying Bilan Carbone® will account for emissions across the full lifecycle of goods and services.

Use Cases and Compatibility

A Bilan Carbone® assessment produces a total carbon footprint (in tonnes of CO2 equivalent), with a detailed breakdown by activity, along with identification of significant drivers of emissions. In addition to supporting France’s BEGES disclosure requirement (described below), the framework assists public and private sector entities in engaging stakeholders and developing targeted decarbonization strategies.

Bilan Carbone® is compatible with other methodologies, most notably ISO 14064 and the GHG Protocol (though there are a number of nuances to boundaries and methodological approaches). At its advanced maturity level, the framework covers most of the ESRS E1 standard for sustainability reporting.

Bilan Carbone®: Key Principles

The Bilan Carbone® oversight agency, ABC, lists nine foundational principles that are embedded in the Bilan Carbone® methodology:

- Consistency: The approach is aligned with current domestic and international strategies to combat climate change (e.g., France’s National Low-Carbon Strategy, Paris Agreement, etc.), and promotes the transition to a low-carbon society.

- Accuracy: The biases and uncertainties inherent in the approach are identified, quantified, and reduced as much as possible.

- Significance: The approach seeks to cover as many emissions as possible, and to prioritize the most significant ones.

- Evaluation: The approach must lead to results that can be analyzed, in particular through the assessment guide.

- Transparency: The approach must be sufficiently transparent, and the results obtained must be published on the platform of the Observatoire de la Comptabilité Carbone® en France (OCCF).

- Low-Carbon Strategy: The approach seeks to add a mitigation dimension to an organization’s strategy.

- Long-Term Vision: The approach helps define the organization’s long-term vision for low-carbon transition.

- Anticipation: The approach encourages anticipation of future changes.

- Pragmatism: The approach requires organizations to stay pragmatic about results, even unanticipated ones.

.png)

What are the latest updates to Bilan Carbone®?

The ninth version focuses on transition planning.

Since it was first introduced, Bilan Carbone® has continued to evolve. Its latest iteration, published in July 2024, brought a more structured methodology with a greater focus on transition planning.

Key developments include:

- Three maturity levels (Initial, Standard, Advanced) to adapt the approach based on organizational capacity, covering scope, frequency, and level of engagement.

- Stronger focus on transition planning, with the method structured as a seven-step process emphasizing action and continuous improvement.

- Shift from stakeholder awareness to stakeholder mobilization, requiring ongoing engagement and participation across the organization.

- Improved uncertainty estimation, combining quantitative and qualitative approaches to better reflect data accuracy and support decision-making.

- Compatibility with major standards, including ISO, the GHG Protocol, French regulatory requirements, and the CSRD framework.

- Optional evaluation and auditing of results, enabling verification, compliance support, and improved transparency.

- Updated format, with a more accessible, structured “wiki-style” methodology and a shorter summary version available.

- Ongoing development, with planned updates covering product and territorial footprints, as well as treatment of avoided and sequestered emissions.

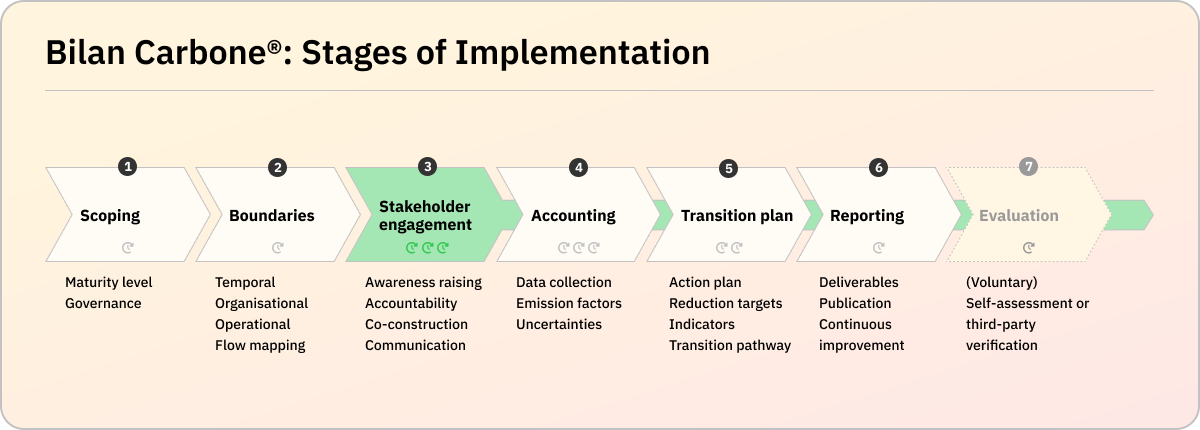

A roadmap for implementing Bilan Carbone®

Companies can follow clear steps to apply the methodology.

Bilan Carbone® is structured into stages, which an organization can use as a practical roadmap for implementation. The approach aims to embed carbon accounting into an entity’s strategic planning, rather than treating it as a one-off compliance exercise.

The seven stages outlined by ABC are:

Stage 1: Scoping

Assess your organization’s maturity level with regard to carbon accounting and climate transition plans. The framework offers different guidance for beginner, intermediate, and advanced maturity levels.

Stage 2: Boundaries

Define your organizational, temporal, and operational boundaries. Identify transition risks and opportunities.

Stage 3: Stakeholder Engagement

Make all stakeholders aware of the Bilan Carbone® assessment and transition plan, and enable them to take action.

Stage 4: Accounting

Collect all activity data and use emission factors to calculate tonnes of CO2 equivalent.

Stage 5: Transition Plan

Plans should include emission reduction objectives, detailed and quantifiable actions, a credible pathway to achieving objectives, and monitoring indicators.

Stage 6: Reporting

The Bilan Carbone® assessment is designed to provide a report that can be shared with stakeholders and regulators. Deliverables include a summary of emissions inventory (broken down by category within the appropriate boundaries), a transition plan, and associated monitoring indicators.

Stage 7: Evaluation

In this optional stage, organizations can engage independent assessors to audit the Bilan Carbone® report using a strict framework.

Source: Bilan Carbone® Methode

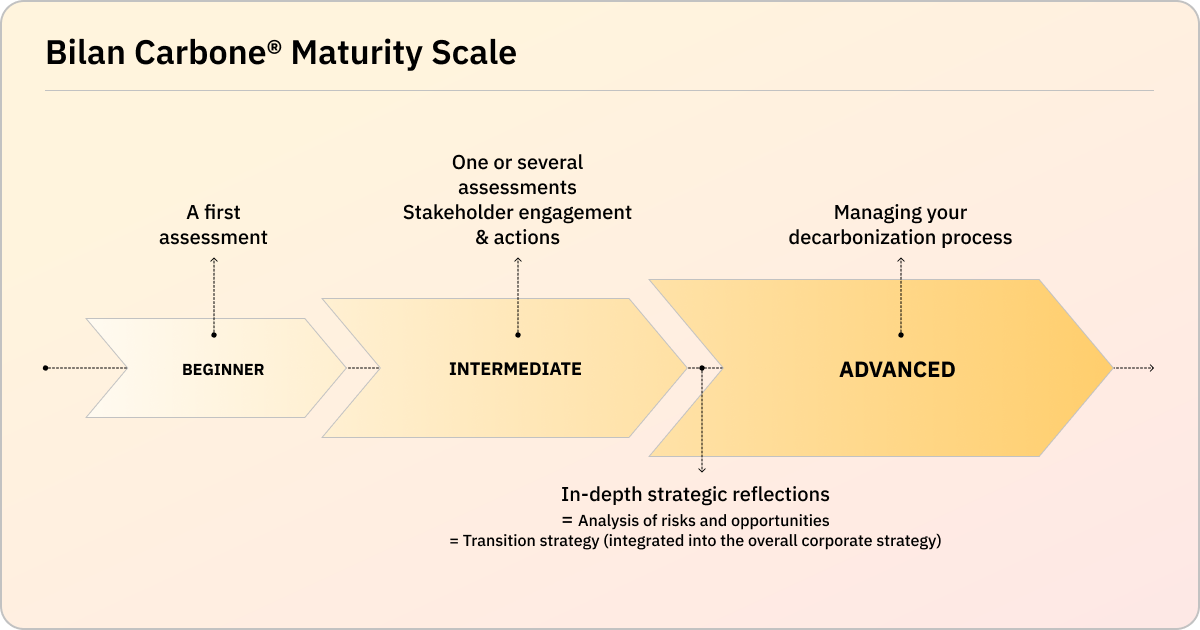

What is the Bilan Carbone® Maturity Scale?

Requirements align with an organization’s carbon accounting maturity level.

In the scoping stage, an organization uses a questionnaire to determine its carbon accounting maturity level, then follows a set of corresponding requirements. The idea is for users to progress in maturity with each iteration (though this doesn’t necessarily mean they will step up to the next level). The stages are:

Initial/Beginner: Initial carbon footprint assessment and a simple transition plan with short-term objectives.

Standard/Intermediate: Comprehensive carbon accounting, with a complete transition plan and medium-term objectives. Full stakeholder engagement.

Advanced: In-depth accounting of the most significant emission categories. A detailed analysis of transition risks and opportunities.

What is Base Carbone®?

Base Carbone® is a public database of emission factors.

Emission factors (EFs) are the foundation of carbon accounting. An emission factor is a representative value used to quantify the greenhouse gases associated with a specific economic activity. When multiplied by activity data (e.g., gallons of gasoline used in business travel), emission factors can provide a clear picture of the carbon impact of products and processes used by a company. Agencies like the IPCC and the US EPA have compiled databases of emission factors, each with its own specific methodology and applications.

Base Carbone® is France’s official emissions database and is a core element of Bilan Carbone®. The database is managed by ADEME, France’s environmental agency, and is used for carbon accounting across sectors.

Because the database is managed by the government and regularly updated, its use can help ensure methodological consistency.

Is Bilan Carbone® mandatory? What is BEGES?

Bilan Carbone® helps entities to comply with BEGES (French GHG disclosure law).

Bilan Carbone® is not compulsory itself. Rather, it’s an approved methodology that enables organizations to comply with French climate disclosure regulations.

The Grenelle II law of 2010 (Article 75) of the French Environmental Code requires certain entities to report their emissions and identify reduction strategies. Bilan Carbone® allows these organizations to complete a compliant greenhouse gas assessment, known as BEGES (Bilan des émissions de gaz à effet de serre), using Base Carbone® emission factors.

The BEGES reporting obligation applies to:

- Companies with more than 500 employees in mainland France (or more than 250 employees in overseas territories)

- Local authorities with more than 50,000 inhabitants

- Public bodies and state institutions employing more than 250 staff

These entities must:

- Carry out a greenhouse gas emissions assessment (BEGES)

- Update it at least every four years

- Publish the results, typically via a platform managed by the French government (ADEME)

Failure to comply can result in administrative penalties (historically up to €1,500, though enforcement frameworks have evolved).

Evolving from measurement to action

One of the central objectives of Bilan Carbone® is to move organizations from measurement to action. To support this approach, the framework focuses on cultivating engagement among stakeholders, identifying emission reduction opportunities, and implementing effective transition plans. A Bilan Carbone® assessment is more than a reporting exercise; it’s an opportunity to embed climate considerations into every aspect of the business strategy.