In February 2026, Korea issued ISSB-aligned disclosure standards, along with a roadmap for implementation. Under the Korean Sustainability Disclosure Standards (KSDS), the largest companies listed on the Korea Composite Stock Price Index (KOSPI)—those with consolidated assets over ₩30T KRW (~$20.4B USD) would have to begin reporting scope 1 and 2 emissions in 2028. The next phase, companies with more than ₩10T KRW (~$6.8B USD), would report starting in 2029. Scope 3 reporting has been delayed by three years.

Korea has joined the global wave of jurisdictions adopting ISSB-aligned climate disclosure standards. The Korean Sustainability Disclosure Standards (KSDS) require companies to report on climate-related governance, strategy, risk management, and metrics, including emissions, starting as soon as 2028.

Below, we provide an overview of Korea’s standards and steps companies can take to prepare for compliance.

Background: What are the ISSB Standards?

Two standards, IFRS S1 and IFRS S2, provide a global baseline for climate disclosure.

The Korean Sustainability Disclosure Standards align with widely-recognized standards from the International Sustainability Standards Board (ISSB). The ISSB was formed in 2021 by the International Financial Reporting Standards Foundation (IFRS), with the goal of creating a global baseline for sustainability reporting. The ISSB issued two core standards: IFRS S1 (General Requirements for Disclosure of Sustainability-related Financial Information) and IFRS S2 (Climate-related Disclosures), which have shaped environmental reporting regulations around the world. To date, more than 30 jurisdictions have partially or fully incorporated the ISSB standards, or are in the process of doing so.

The ISSB built IFRS S1 and S2 on the foundation created by the Task Force on Climate-Related Financial Disclosures (TCFD). The standards also draw on frameworks from the Climate Disclosure Standards Board (CDSB) and the Sustainability Accounting Standards Board (SASB).

Though ISSB has shaped policies in dozens of countries, it is an independent standard setter, not a regulatory body. The organization does not impose reporting requirements on any jurisdiction or company. Its standards are designed to provide a structure for consistent and comparable regulations across borders.

What are the Korean Sustainability Disclosure Standards?

The KSDS standards closely follow IFRS S1 and S2.

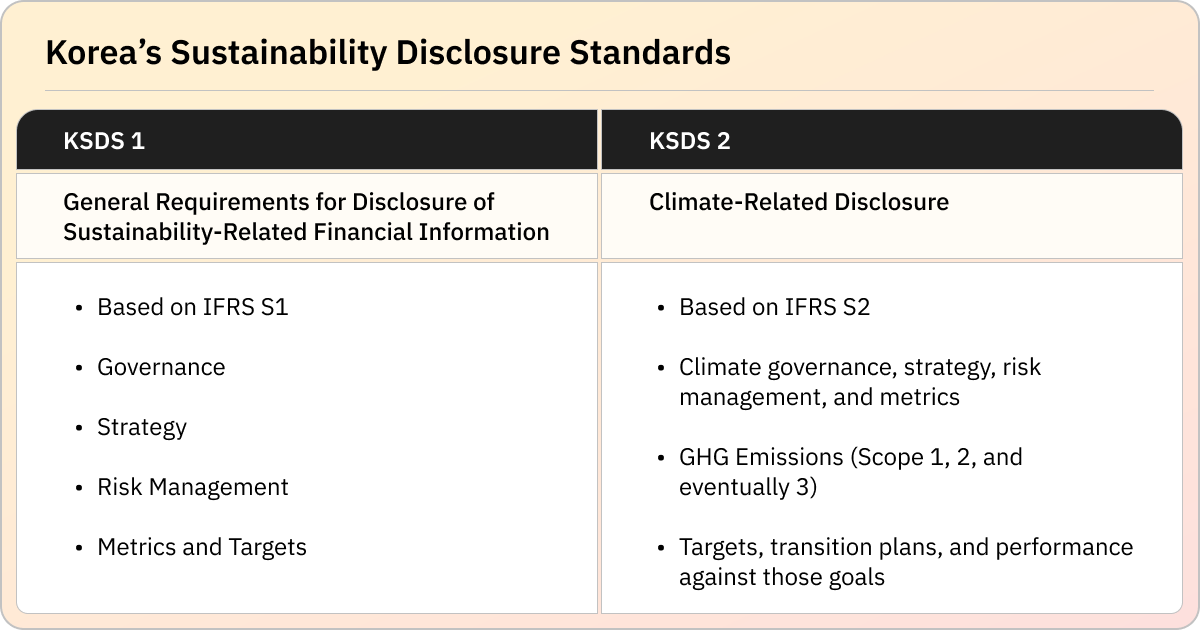

On February 26, 2026, the Korea Sustainability Standards Board (KSSB) published the approved Korean Sustainability Disclosure Standards (KSDS). The framework consists of two standards:

KSDS 1: General Requirements for Disclosure of Sustainability-related Financial Information

This standard is based on IFRS S1 (General Requirements), and requires reporting on:

- Governance over sustainability-related risks and opportunities

- How sustainability issues affect the business model, strategy, and decision-making

- Risk management processes for identifying, assessing, and managing sustainability-related risks

- Metrics and targets used to monitor and manage sustainability-related risks and opportunities

KSDS 2: Climate-Related Disclosure

The second standard is based on IFRS S2 (Climate-related Disclosures), and covers reporting on:

- Climate-specific governance, strategy, risk management, and metrics/targets

- Climate-related risks and opportunities (transition and physical risks)

- Greenhouse gas emissions (scope 1, 2, and 3)

- Targets, transition plans, and performance against those goals

KSDS 1 and KSDS 2 are intended to be applied on a mandatory basis. Until mandatory requirements take effect, entities may voluntarily apply the standards from the beginning of the annual reporting period in which they are issued.

Dropped - KSDS 101: Additional Disclosure Aligned with Policy Objectives

The initial 2024 KSDS exposure drafts included a proposed third standard, KSDS 101, which would have addressed additional sustainability-related information required by domestic laws or to meet Korea-specific sustainability policy objectives. However, the KSSB decided not to issue KSDS 101 in the final standards, citing changes in the government policy environment and the potential burden on companies.

What is the KSDS roadmap?

Korea’s FSC has issued implementation guidance for the standards.

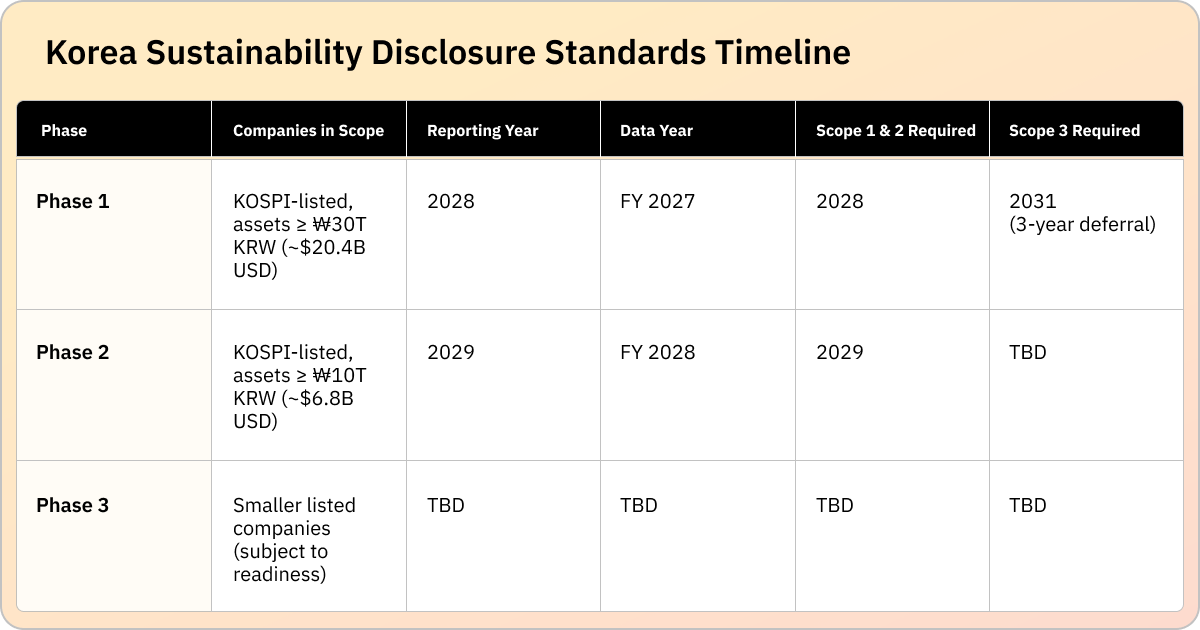

On February 25, 2026, Korea's Financial Services Commission (FSC) released a draft roadmap for mandatory sustainability disclosures. The roadmap was published alongside the finalized KSDS and lays out an implementation timeline, with reporting proposed to begin in 2028 for the country's largest listed companies, and scope 3 reporting for that group delayed until 2031. A full implementation timeline is provided below.

Who is subject to Korea's sustainability standards?

Requirements begin with the largest KOSPI-listed companies and expand over time.

Under the proposed roadmap, mandatory sustainability reporting will apply initially to companies listed on Korea's benchmark KOSPI Index (Korea Composite Stock Price Index) with consolidated assets exceeding ₩30T KRW (~$20.4B USD). These are the very largest companies on Korea's main exchange.

The roadmap envisions expanding requirements to KOSPI-listed companies with assets above ₩10T KRW (~$6.8B USD) one year after the initial phase. Further expansion to smaller KOSPI-listed firms remains possible, subject to market readiness and international developments.

The intended users of disclosed information are existing and potential investors, lenders, and other creditors, which is consistent with the focus of ISSB Standards.

What is the timeline for disclosure?

The first disclosures are due in 2028, based on 2027 data.

Under the timeline proposed by the FSC, large, publicly-listed companies (those with more than ₩30T KRW/$20.4B USD in assets) will have to begin reporting scope 1 and 2 in 2028, using FY2027 data, and scope 3 in 2031. The next wave (publicly-listed companies with more than ₩10T KRW/$6.8B USD in assets) would begin reporting scope 1 and 2 in 2029 using FY2028 data, with scope 3 deadlines still to be determined. Mandatory reporting deadlines for smaller listed companies have not been issued. Until mandatory requirements take effect, companies can choose to apply the KSDS voluntarily.

What are the key features of Korea’s sustainability standards?

The KSDS follow the ISSB model closely, with several modifications.

While the KSDS are based directly on IFRS S1 and S2, the finalized standards include some notable modifications. Authorities note that the KSDS were designed to reflect the real-world circumstances of companies in Korea, while ensuring interoperability with ISSB standards. To this end, Korea has made certain requirements optional, introduced a reporting exemption, and extended the timeline for scope 3 reporting. Korea has signaled that it will gradually increase alignment with the ISSB, taking into account implementation experience, investor demand, and international developments.

Key features of Korea’s current framework include:

Climate-First Approach

IFRS S1 includes a one-year transition relief allowing companies to initially focus on climate-related disclosures before reporting on other sustainability risks. KSSB takes this further, making climate-related disclosure the sole mandatory focus of the standards. Disclosures on other sustainability-related matters are voluntary under the current framework, with no specified timeline for expansion. If companies want to report on other sustainability issues, they can do so under KSSB 1 Appendix E “Disclosure requirements for core content.”

Scope 3 Reporting Extension

KSSB has confirmed a three-year deferral for scope 3 reporting, giving companies additional time to build the infrastructure required for value chain emissions data collection and measurement.

Financial Statement Exemption

Korea has issued an exemption that allows companies to publish their sustainability reports at a different time from their financial statements. The ISSB Standards call for simultaneous publication.

Industry-Based Metrics (Optional)

Under Korea’s standards, companies can voluntarily decide to disclose industry-based metrics. While KSSB recognizes that industry-specific data is useful for stakeholders, it has noted that this type of information is currently unclear due to the absence of consistent industry standards. It has therefore made reporting optional. Authorities will determine the timing of future mandatory industry-based metrics after consideration of how international industry standards have developed, along with domestic readiness.

Internal Carbon Prices (Partially Optional)

KSDS 2 requires companies to disclose whether and how they use internal carbon prices, but leaves disclosure of the specific price per metric tonne of GHG emissions optional. Korean authorities will determine whether and when that price disclosure becomes mandatory in the future, based on international developments and domestic conditions.

Third-Party Assurance (Optional)

The FSC roadmap proposes that third-party assurance begin as optional, with mandatory adoption to be considered gradually in line with global trends.

Phased Enforcement

Korean authorities have suggested a phased approach to enforcement, with an initial focus on guidance and support rather than penalties or sanctions. Under the proposal, companies will be exempt from civil damages and administrative penalties during the first two years of mandatory reporting, with no criminal liability during the initial phase.

Why is Korea adopting ISSB-aligned standards?

Alignment establishes a baseline to help companies meet global expectations.

Korea’s adoption of ISSB-aligned standards is part of a larger global trend of alignment and comparability. Korean authorities note several important factors driving their disclosure laws:

- Interoperability with global standards. Korea’s FSC has stated that domestic standards should be "congruent with global standards (such as ISSB Standards) and interoperable with the sustainability disclosure standards of major economies, taking into account particular characteristics of domestic industries and business operating conditions." The KSSB has echoed this, noting that the KSDS were designed to "ensure interoperability with IFRS S1 and IFRS S2" while reflecting Korea's disclosure environment and companies' practical circumstances.

- Reducing the burden on companies. One of the stated goals is to minimize dual reporting burdens for Korean companies that operate internationally. By aligning domestic standards closely with the ISSB baseline, the FSC aims to reduce the complexity of reporting across multiple jurisdictions.

- Supporting Korea's green transition. The FSC has linked the sustainability disclosure framework to Korea's broader green transition agenda, positioning mandatory reporting as part of transition-related market infrastructure rather than a standalone transparency exercise.

- Active participation in global standard-setting. Korea has been reappointed to the IFRS Foundation's Sustainability Standards Advisory Forum (SSAF) for 2026–2028, represented by both the FSC and the KSSB. The FSC notes that participation in the forum will further facilitate the sharing of domestic implementation concerns on the international stage and help build consistency between domestic reporting practices and international standards.

How can companies prepare for KSDS reporting?

Building strong data foundations now will streamline disclosure when requirements take effect.

If your company falls within the scope of Korea's proposed sustainability reporting requirements, mandatory disclosure could kick in as soon as 2028, and preparation should begin well before then. Here are steps you can take to streamline your KSDS reporting:

1. Assess your current reporting baseline

Start by identifying any existing sustainability reports, CDP disclosures, or other documents where you've already disclosed climate-related risks and opportunities. Map that information against the KSDS 1 and KSDS 2 requirements. You'll want to document any gaps you find, especially in areas like scope 1 and 2 emissions measurement and climate scenario analysis.

2. Build a foundation for reliable data management

Like IFRS S2, Korea's standards require measurable, auditable data, not just narrative descriptions. It’s important to establish clear data ownership across teams (e.g., sustainability, procurement, finance, operations) early on. Make sure to select appropriate data management tools and review emissions calculation methodologies for consistency with recognized GHG accounting standards.

3. Integrate climate risk into strategy and planning

Identify climate-related risks and opportunities that could reasonably affect your company’s financial performance, position, or future prospects. Make sure to align this assessment with your existing enterprise risk management and financial planning processes.

4. Start building toward scope 3 readiness

While Korea's roadmap provides a three-year deferral before scope 3 reporting is mandatory, value chain data is notoriously challenging to collect. Teams should start engaging suppliers and mapping scope 3 categories well in advance to avoid a last-minute scramble when the requirement kicks in.

5. Establish governance and internal controls

With mandatory reporting comes increased scrutiny. It’s essential to clearly define roles and responsibilities for data collection, review, and approval. Make sure you understand and document the emission factors and methodologies used for calculations and begin preparing for the eventual introduction of third-party assurance requirements.

6. Monitor the roadmap finalization

While the standards are final, the implementation framework is still subject to confirmation. The FSC conducted a public consultation on the draft roadmap and is expected to finalize it in 2026. Companies should continue to monitor official FSC announcements for updates on reporting entities, timing, disclosure channels, and assurance requirements.

Laying the groundwork for confident KSDS reporting

Now that Korea’s standards are final and an implementation plan has been published, in-scope companies should have a clear picture of what they’ll need to report. By beginning to build data management systems, governance structures, and emissions reporting capabilities now, teams can approach 2028 with confidence and lay the groundwork to readily adapt as requirements expand over time.

FAQs

How does Korea’s framework align with ISSB standards?

Korea's KSDS 1 is based on IFRS S1 (General Requirements for Disclosure of Sustainability-related Financial Information), and KSDS 2 is based on IFRS S2 (Climate-related Disclosures). For more information, see the IFRS Foundation’s jurisdictional snapshot.

What is KSDS 101?

The initial 2024 KSDS exposure drafts included a proposed third standard in addition to KSDS 1 and 2. KSDS 101 would have addressed additional sustainability-related information required by domestic laws or to meet Korea-specific sustainability policy objectives. However, the KSSB decided not to issue KSDS 101 in the final standards, citing changes in the government policy environment and the potential burden on companies.

Which companies are required to report?

Under the proposed roadmap, KOSPI-listed companies with consolidated assets exceeding ₩30T KRW/~$20.4B USD are required to begin reporting in 2028 based on 2027 data. This is expected to expand to companies with assets above ₩10T KRW/~$6.8B USD in 2029, with potential further expansion to smaller firms subject to readiness and international developments.

When does Scope 3 reporting become mandatory?

Under the proposed roadmap, mandatory Scope 3 value chain emissions reporting for large companies is deferred by three years from the initial start of mandatory reporting, to 2031. This provides additional time for companies to build the necessary reporting infrastructure.

Is third-party assurance required?

Initially, third-party assurance will be optional. The roadmap proposes a gradual movement toward mandatory assurance in line with global trends.

Can companies apply the KSDS voluntarily before mandatory requirements take effect?

Yes. Entities may voluntarily apply the KSDS from the beginning of the annual reporting period in which they are issued.